Stocks

-

The Japanese P&C carrier agreed a deal to buy 15% of WR Berkley shares in March.

The Japanese P&C carrier agreed a deal to buy 15% of WR Berkley shares in March. -

The investor offloaded nearly 100,000 Allstate shares in Q3, according to its latest 13-F.

-

The $21/share pricing falls in the middle of the expected range.

-

Fears of the oncoming soft market are causing a sector rotation away from P&C.

-

The CEO noted that 45% of Everest’s US casualty book did not renew this quarter.

-

The selloff may hint at headwinds for equity investors.

-

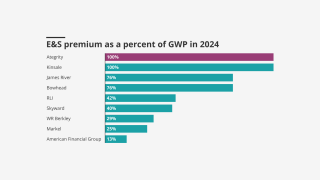

E&S is most exposed to growth normalization, private credit is hunting P&C and fronting is deadlocked on exits.

-

Industry stocks were firmly behind the S&P 500 in Q3.

-

The Japanese carrier has agreed to buy Aspen for a realization of $3.5bn.

-

The insurer has chosen a “take two” deal after buying Endurance, betting again on Bermuda.

-

Third Point purchased 50,000 shares of the E&S insurer, which represents roughly 0.1% of its shares outstanding.

-

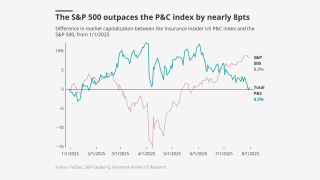

The S&P 500 outperforms as P&C tumbles on mixed earnings.

-

The president expects to see benefits from the deal in H2 2026.

-

Brown & Brown fell 10% and Ryan Specialty 8% as investors digest the deteriorating outlook.

-

The broker posted a 6.5% drop in organic growth YoY.

-

P&C’s outperformance lead dwindles, while specialty rises above other segments.

-

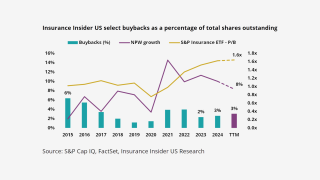

Additional buybacks are more feasible if P&C stocks slip and pricing moderates.

-

Above-market organic growth, mid-market M&A and talent infusions were all heralded.

-

The aggregate gross proceeds from the offering are expected to be $113.3mn.

-

Insurance outperformance slows as markets recover from tariff shock.

-

The latest E&S player planning to IPO remains a “show me” story.

-

Unpacking how much excess capital there really is and dissecting the source of its returns.

-

The program will succeed the previous buyback launched in 2023.

-

The conglomerate’s insurance subsidiaries will have to make do without some of their prior strategic advantages.