Frady, the CEO of Hazard Hub, is on a mission to collect the location of every fire hydrant in the US.

Hazard Hub now has around 11.2 million hydrants in its database, but collecting the hydrant locations is a Sisyphean task: the number rises constantly as new properties are built and road networks expand.

“Every week we add about 20,000 hydrants,” says Frady, who has gone from plotting the locations by himself when he founded the company in 2016, to having a team of people hunt hydrants for him.

Welcome to the data market, where vendors supply insurance companies with a bewildering array of information, for a price. Frady is part of network of data vendors that buy, sell, aggregate and structure the data that underpins automated digital underwriting in the P&C market.

Ever since the Lloyd’s List started publishing shipping news in late 17th century London, underwriters have had an insatiable appetite for data. Now new technology, some of it developed by Lloyd’s Lab participants like Hazard Hub, is leading to radical changes in how risks are underwritten and how claims are paid across the industry.

Frady is adamant that it is pointless for an insurer to be asking a client where their nearest fire hydrant or fire station is located – the carrier should know already.

“It’s a dumb question to ask,” he said.

The chances are that if you are reading this story in a home or office, some insurance companies will already know more about that building than you do.

They shouldn’t need to ask you what the roof is made of, or when that location was last hit by a cat event, when you apply for coverage, because these essential data points are now being built into underwriting engines.

“You make a great insurance buying experience by eliminating a lot of the junk like where's the fire hydrant? Where's the fire station? These are stupid questions. All of these questions can be pre-populated,” said Frady.

“What our customers have been seeing is that if you eliminate these dumb questions you can focus on the smart questions that mean something to the insurers.”

Data gaps

Rapid advances in the quality of aerial imagery allow insurers to collect hyper-localized data at scale in a way that just would not have been possible even a few years ago.

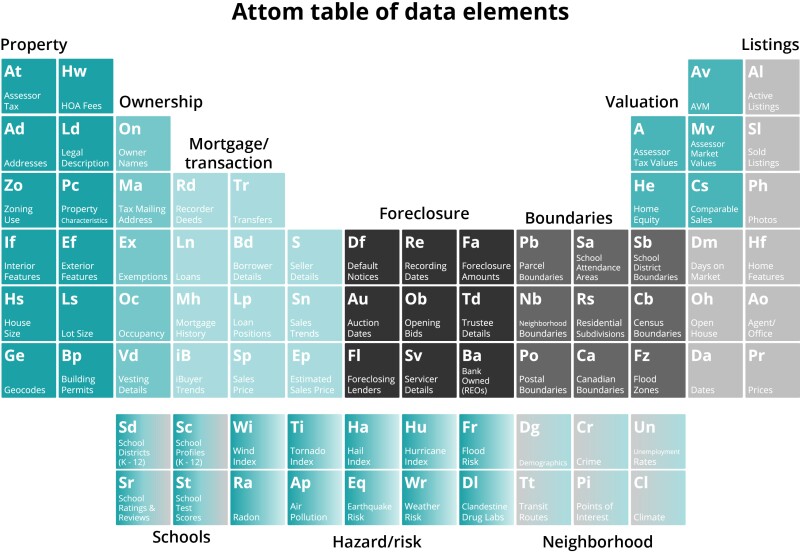

Rob Barber, CEO of Attom Data Solutions, points out that insurers are now using aerial data sets to work out the height the trees on the perimeter of a property

“They will calculate if there's a windstorm and the tree falls, is it going to land in the yard, or is it going to land on the roof?”.

Casualty risk can also be ascertained from the sky. Trampolines – a litigation magnate - can be spotted from space. Barber said one client is using aerial imagery to work out if swimming pools are fenced off, or open to the garden, an underwriting metric which effects the premium paid for an umbrella casualty policy.

As Hippo’s chief product Officer Aviad Pinkovezky puts it: “There are some gaps in traditional data sources that prevent you from understanding defined nuances about the property at scale.”

Take the tricky issue of vegetation around a property in a wildfire zone.

Pinkovezky said using satellite data “opens up a whole new opportunity for us to have meaningful interaction with customers”.

Using data from Cape Analytics, he said, Hippo can assess whether there is vegetation 10 feet or closer to the house that could worsen the home’s chances of surviving a wildfire.

“Then we can actually advise the customer what to do in order to mitigate potential fire hazard”.

Climate data

Satellite data can also help insurers craft parametric coverages. Swiss Re has developed a product to indemnify farmers against the risk of a drought, with help from Dutch startup VanderSat.

The Swiss reinsurer is now able to tell whether the soil moisture level in a particular location has gone far enough outside of the standard deviation to warrant a drought claim being paid.

Swiss Re is tapping satellite data from NASA and the European Space Agency (ESA) to run the program.

Swiss Re senior underwriter Marcel Andriesse points out that while in the past, one had a low-resolution picture of the planet available every 20 days, newer technology is changing the game.

He noted that the that the ESA’s Copernicus satellite network now gives an image of the whole world, to a 5m to 10m (16 ft – 32 ft) resolution.

“This is a dream,” Andriesse says. “It’s a fantastic satellite program, it has such good coverage, such good resolution.”

Having the right data – and the right technology and analytics partners – allows Swiss Re to help cedants find new ways of indemnifying perils that were prohibitively costly to loss adjust in the past.

The data market

A sophisticated ecosystem of data providers has emerged. Data providers like Attom act like wholesalers to clients - whether they are software companies, insurers or banks - who feed structured data into their systems to mine for insights and guide decision making.

The calculus for insurers must be whether the benefit to the loss ratio and expense ratio of using new data sources, outweighs the costs of accessing the data in the first place.

Attom CEO Barber said a client told him recently that if the data they put to use to create analytics ends up reducing their need to set aside reserves to cover future losses by 1%, that 1% “could be hundreds of millions of dollars”.

Using novel data sources can have an “outsized financial implication, down the road if you can do it well,” Barber said.