Crossing the billion-dollar threshold was perhaps inevitable after years of dramatically escalating so-called “nuclear” verdicts, but the size of the award nevertheless raised eyebrows as the latest indication of runaway social inflation.

“It’s a sign of what’s coming down the road,” said Bob Greenebaum, CRC Group casualty practice group leader and central region director.

Multiple factors are playing into the increased frequency of severe liability losses, pegged at $15mn or more. Litigation financing, the increased use of class-action lawsuits and growing distrust of corporations are all fueling higher verdicts in cases that make it to court.

“They’re awarding $300mn for an auto claim that 10 years ago would have been $500,000,” explained Andrew Grim, national casualty practice leader for Brown & Riding.

And this has become a self-reinforcing trend. Juries don’t need to be involved for losses to expand because higher verdicts are leading to higher settlements, as insurers try to forestall awards.

Greenebaum noted that cases insurers would have taken to court a decade ago with a reasonable expectation of victory are now being settled out of concern that litigating the claim would take years and could result in a nuclear verdict.

“Underwriters are very concerned,” echoed Anthony DeFelice, Aon’s managing director for national casualty. In recent months, the broker recorded a $126mn loss and another close to $60mn. “These are actual settlements, not jury awards that could be overturned,” he noted.

“I see these losses coming through the system and they’re just huge,” DeFelice continued. “And they’re going to impact the system.”

Neil Smallcombe, head of casualty at AIG’s Lexington Insurance unit, likened nuclear verdicts to escalating catastrophe claims in the property market. “This is not a weather-the-storm situation, this is a new normal,” he explained.

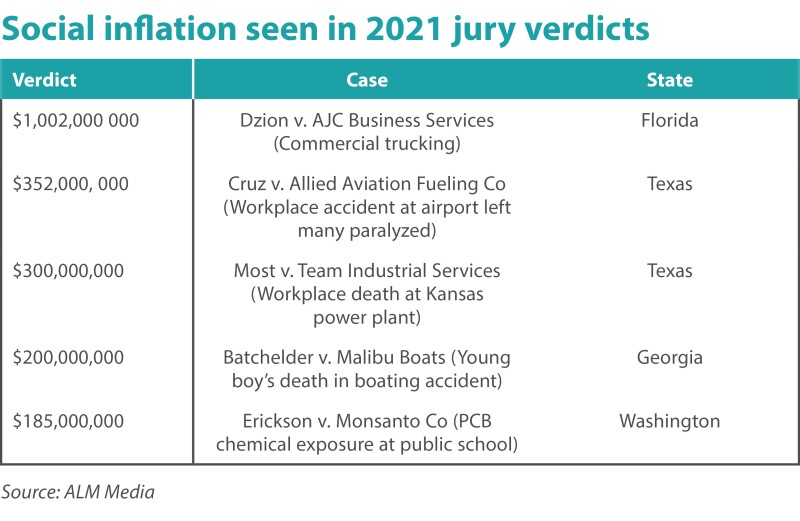

Year to date, Smallcombe said this year, the excess casualty market has recorded 15 verdicts greater than $25mn, nine higher than $50mn and five that topped $100mn, including one in recent weeks for $143mn. These numbers are well down on pre-pandemic levels when Verdict Search data shows 102 $20mn+ verdicts in 2019.

However, these are the numbers that have been recorded during a period when the impression has been that the threat has gone into deep freeze as a result of the pandemic – and the pace is picking up.

“I view it a bit of a forerunner of what’s to come in 2022,” Smallcombe said. “I think perhaps there’s been a bit of a reprieve, or a blind spot, because of the court systems being closed [during the pandemic].”

As courts resume normal operations, there’s pressure coming from judges to clear case backlogs, AIG’s Smallcombe added. “As much as ‘social inflation’ is this sort of well-worn phrase now, I think a lot of it’s still hidden, because of how slow the court system has been moving the last 20 months or so,” he stated. “I think it’s just the beginning.”

The impact of social inflation on industry reserve adequacy, particularly for the soft 2014-18 accident years, was the dominant theme of 2019 and a key driver of the upward inflection point that pricing hit as insurers tried to get on top of loss-cost inflation.

A return to high volumes of nuclear awards, including a “catch up” phase when the backlog is cleared, would have a major impact on underwriting profitability in 2022, and on sector sentiment.

Smallscombe said another confirming feature of what was being seen now was the spread of these kind of verdicts from states like California, Florida, Illinois, Georgia and Texas into areas like Kentucky and Utah where they have not been seen before.

There’s not much that the insurance industry can do to quell the increases, pointed out Alan Rodrigues, executive underwriting officer for casualty at Markel Insurance. One possibility is to lean more heavily on mediation to try to keep the cases out of the courtroom.

“The larger issue is the impact of media and social media on people’s perception of what is fair and equitable,” observed Sean Hickey, NFP's senior vice president of risk management services. He acknowledged that there’s an emotionally charged environment right now.

“I think juries are really stepping deeply into the shoes of the injured parties,” he said. But he noted that some of the awards are so large that there might not be enough insurance capacity to make good on the verdicts.

“While there have always been large awards, I think there’s a level of proportionality that far outstrips what we’ve seen in recent years.”

The size of the awards also keeps raising the bar for what’s expected in subsequent cases, according to John Ferguson, head of excess casualty at Zurich North America. The ramifications are widespread, he said, because the nature of the insurance industry means rates will continue to rise if payouts carry on increasing.

Rate increases are moderating

After several years of rapidly accelerating rates, the increases slowed in 2021.

DeFelice said that, across his entire book of business within Aon, the average rate increase was 15% in the third quarter. “It’s well down from last year, dramatically down from last year.”

Most of the increase, in fact, came from the most challenged parts of the book, about 20% of which had average rate increases of 43% (down from about 51% in Q3 2020). But across the other 80% of the portfolio, the average increase was just 5%. And for many clients – those without difficult exposures and good loss histories – rates went negative.

CRC’s Greenebaum saw a similar average of 16% increase among his clients, whereas 18-20 months ago, some classes recorded 100%-200% spikes. “If you got 100% last year, you might get away with 20% this year,” he noted.

New capacity has entered the market now that rates are more aligned with loss expectations. “Everything got more attractive and new capital was attracted into the space,” Greenebaum explained. However, he added, the new capital is not driving down rates. “It’s not naïve capital,” he said.

Instead, he attributes the deceleration of pricing to rate adequacy.

“New carriers are starting conservatively,” Brown & Riding’s Grim agreed. “While they may be filed for $25mn of capacity, they’re being prudent on how they deploy it.”

Zurich’s Ferguson said the increased attachment points that accompanied the harder market should remain. “I would love to carry that forward where we’re putting up shorter limits,” he said.

“We’ve seen time and time again that without this discipline, providers get sunk. That’s when seismic change occurs and providers pull in and out of spaces.”

The days of writing lead layers of $50mn are over, he noted. For some legacy accounts, $25mn is still possible, “but we’re probably not going to look to it for new business".

Regarding insurers, NFP’s Hickey said: “They’re acting with more discipline than they have in prior decades. There’s not a particularly large amount of wiggle room.”

AIG’s Smallcombe agreed. “Capacity is tightly guarded,” he pointed out, noting that carriers are building more resiliency into their portfolios by moderating their risk appetites.

“The days of any markets being focused on a large limit lead strategy of $25mn, I think they’ll find themselves in trouble in this litigation market,” he explained. “We’re referring to it as a structural shift in the valuation of claims that requires a permanent response to deal with it.”

Greenebaum said it can still be challenging to meet client demands: “The more difficult the risk, the more difficult the tower is to build.”

Among the most difficult verticals are commercial auto and trucking, pharmaceutical and opioid coverage, public entities, multi-family habitational, hotels, residential and New York construction. But any accounts with large losses can fall into that group.

Education and higher education are also tough to place – in part because of abuse and molestation claims. Hickey said there’s also growing concern about athletic programs due to exposure to concussion and traumatic brain injuries. “That’s one area that’s somewhat challenging,” he noted.

Rodrigues pointed out that rate hikes also mean some insureds are forced to opt for less coverage, “Our clients are not buying as much limit as they used to,” he said. “Today, they can buy only $500mn limits, where two or three years ago, they could buy $1bn for the same cost.”

That’s leaving companies exposed. “The hardening market over the last two-and-a-half years on excess has been a vicious cycle,” stated Brown & Riding’s Grim.

Wildfire worries spread

One particular area getting new attention is wildfire liability across a swath of western states where it was not a great concern before.

A range of different industries, from utilities to contractors, are affected by the fact that drought conditions have spread from California north and east. This summer there was unprecedented fire activity in Oregon, Washington, Nevada, Arizona, Utah, Montana and Wyoming, creating a more difficult market.

“There obviously is a whole range of different industries affected by it,” pointed out DeFelice, naming not only utilities but forestry management operations, electric contractors and more.

Markel’s Rodrigues said even small businesses like tree-trimming services are facing huge costs because of these concerns. “We’re finding some of these smaller contractors or landscapers being asked to carry $500mn,” he pointed out. “The wildfire casualty market is really challenging.”

DeFelice said securing coverage for clients with exposure to wildfire had become problematical in the last few years. “The rate on those lines is outrageous,” he stated, noting that they’ve paid out billions in losses.

While California is still the epicenter of wildfire concern, he continued, “these other states are really on the radar as well now”.

And it’s not only wildfire that’s getting attention. Last February’s Winter Storm Uri in Texas brought a range of risks to the forefront.

“Climate change is here to stay,” Greenebaum noted. “It’s going to create bigger losses.”