Until now, private broker valuations had enjoyed an upward trend, which pushed average Ebitda multiples to 17x-18x – levels seen in recent billion-dollar deals, such as Foundation Risk Partners.

This positive trend was mostly driven by the combination of significant tailwinds from both the pricing cycle and a frothy market, driven by a late-pandemic bounce-back.

Now, despite a weaker economic outlook, market participants canvassed by this publication said they still would not be surprised to see multiples creep higher to around 18x-19.5x Ebitda for private brokers, before seeing some sort of correction.

It is understood that mid-market transactions, for instance – where valuations are currently in the mid-teens – may also see multiples increase to around 17x Ebitda.

Further, recent reports indicate that M&A activity has rebounded after a slow Q1.

Last week Reagan Consulting reported that transactions in the brokerage space rose over 10% to 119 in Q2. The firm said there wasn’t any indication that M&A interest has diminished from either buyers or sellers.

Yet, while some sources do expect that a correction will happen eventually, others said private broker multiples will remain high compared to previous years, unless financial markets collapse, which they deem unlikely.

“The high valuations that we see today it's not a balloon that's going to pop,” said John Wepler, chairman and CEO of insurance-focused investment bank MarshBerry. “It's a new normal.”

Tuck-ins

Tuck-in acquisitions remain an effervescent corner of the market, as buyers still have cheap money undeployed – a result of significant refinancing in 2020/2021, the use of fixed-rate debt, and the benefits of Libor floors and interest rate hedging.

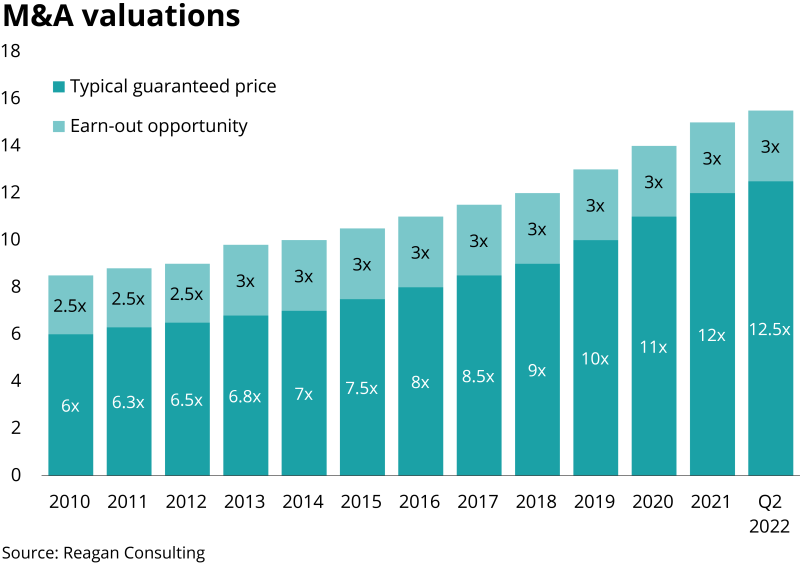

With strong demand from over 50 well-capitalized buyers and still relatively low cost of capital available in Q2, Reagan Consulting recently reported that earn-out multiples being paid by strategic acquirers for a well-run agency with $3mn-$10mn in revenue have risen to around 12.5x.

For larger transactions, multiples have increased to levels described as “unheard of” three or four years ago, with current deals seeing numbers of 14x on average and a few outliers north of 16x Ebitda.

For instance, over the last 12 months through Q2, MarshBerry said brokers with $20mn-$200mn in revenue that transacted saw averaged Ebitda multiples of 13.9x.

The Ohio-based investment bank estimates this figure could increase 20% to 16.7x before average returns fall.

Market participants said some of the factors that could drive valuations up include the industry’s risk perception and current economic conditions.

First: low risk, high returns

Sources in the past have noted that investors in the broking space have been outperforming the standard return targets they have set.

Annual equity returns for those private equity firms backing broking platforms have run in excess of 25%, and it has not been uncommon for returns above 30% to be achieved, sources said.

In fact, one outlier is the recent deal in which Howden acquired Flexpoint Ford-backed reinsurance broker TigerRisk. In this transaction, the Chicagoan PE house booked close to 4x its equity investment in just two years.

These returns explain in part the increasing appetite of PE firms in the insurance broker space.

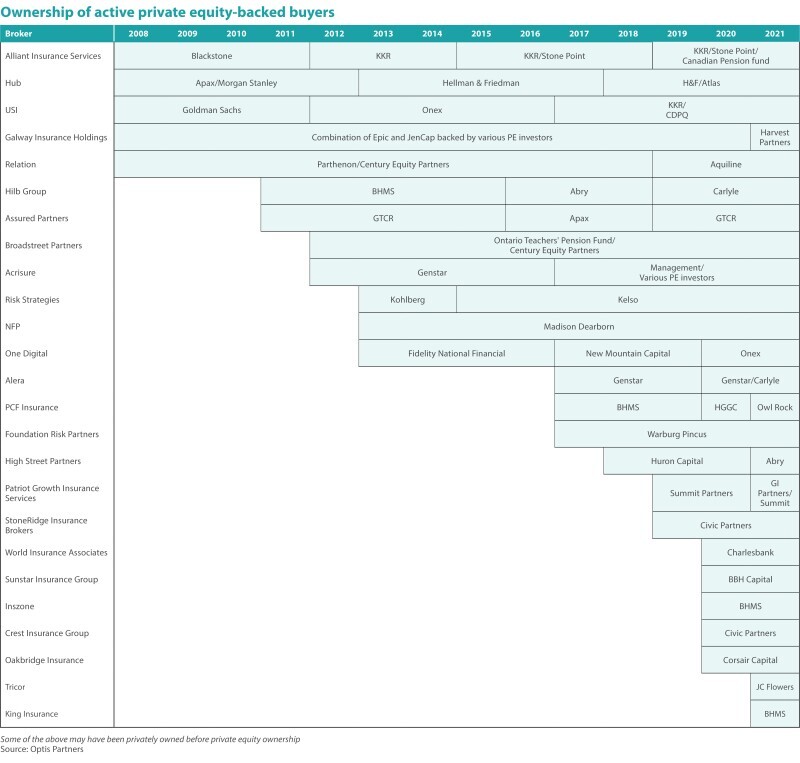

According to MarshBerry figures, last year 703 of 923 announced deals involved private capital-backed buyers, while back in 2005 two of over 200 deals involved a PE-backed firm.

“The number of deals hasn't gone up at all, except private equity has entered the business,” Wepler said.

Back in 2006 only there were seven PE-funded brokers, but that number increased to 43 in 2021.

“In terms of where the market valuation is today, it's being set by private equity,” Wepler added.

The higher-than-expected returns that have drawn private capital to the industry are particularly remarkable given the low risk that insurance brokerage represents compared with other markets, Wepler said.

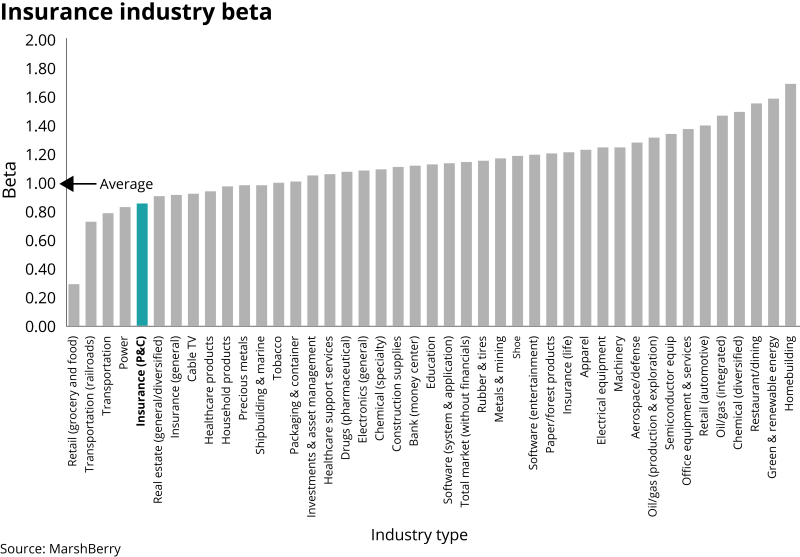

The industry’s beta – a measure of the sector’s volatility compared to all other industries – ranks among the lowest in the economy with an average just above 0.8. Gallagher, for example, is one of the public brokers with the lowest betas in the sector – at 0.68.

This low risk-high reward paradigm has been fueling PE appetite in the industry, driving valuations up over the last years.

Second: economic conditions

It is somehow easy to argue that unfavorable macroeconomic conditions such as beleaguered economic growth, rising inflation and higher interest rates, will lead to a downturn in M&A activity and multiples.

However, these conditions do not necessarily apply to the insurance industry. Sources said that for brokers there is an upward pressure from economic headwinds.

This is because insurance brokers are businesses with high free cash flows and low investment costs.

Moreover, as the economy struggles, investors look for safer ways to deploy capital, making insurance brokers an attractive target.

“You've raised capital and you have to spend it. Would you not start channeling more of your capital into lower beta industries that are less volatile in times of turmoil?” Wepler noted.

Warning signs

Sources warned that for all of Foundation’s defiance of gravity, and the positive intelligence on tuck-in deals, all the factors remain in place for a downward correction in valuations.

Inside P&C has previously argued that greater pressure will come from the debt markets, with interest rates up 225bps already this year, and with more to come. Increased debt servicing costs, reductions in the number of turns of debt put into deals, and the unavailability of dividend recaps will all take their toll.

The private brokers are heavily reliant on debt financing, typically operating with debt-to-Ebitda ratios of 5x-10x, with most in the 7x-9x range, and well ahead of the 2x-3.5x for the public brokers. This cheap leverage has fueled dramatic consolidation plays from these brokers.

This publication has discussed before that after an incredible run over the past couple of years, capping off a great decade, things are set to get harder for the levered private brokers although the space remains fundamentally resilient. (See: Levered brokers: Squeezed returns, but fundamentally resilient.)

One source said that the current perception of low risk in the broking sector together with rising multiples may lead to higher risk-taking, while another source wondered if investors may be underestimating the risk in increasing leverage in the market.

Indeed, leverage could drive a correction and there is always a cyclical component in the market, so some sources expect valuations to finally face gravity after an incredible upward march.

Nonetheless, others said that even when valuations come down, there is a chance they will stay at a much higher clip than in the past.

In addition, the anticipated slowdown in M&A activity may also be less dramatic if the high-yield market becomes more accessible long before the capital raised runs out.

Absent an economic and financial crisis, the most probable scenario is the correction will be smooth for private brokers, sources agreed.