With the heightened effect of social media, the post-Covid bull market made everyone look like a genius. However, the conditions and the stock playbook have completely changed.

As 2022 began, the Fed effectively ended this latest bonanza of cheap-money-fueled speculation by increasing interest rates at the fastest rate in history. Although our 401k’s don’t look as great, we’re happy to see less content boasting trading “strategies” such as using a margin account to buy calls on mid-cap stocks like AMC Theaters or Peloton stationary bikes (remember those?).

With the retail and day traders beginning to take a back-seat over 2022 and inflation spiking higher, the stock market overall began its slow decline over the year. What was hot was suddenly not. Growth stocks/sectors which are closely intertwined with the economic outlook took a beating.

Value sectors such as insurance, which are resilient to a fluctuating economic outlook, came back in favor and consequently ended up outperforming several other stock groups.

In terms of insurance sub-sectors, a majority of the stock performance mimicked market conditions. Specialty players, including the time-tested book value compounders, led the league tables, followed by personal lines players.

On the other hand, Insurtechs and Florida domestics, down double-digits for the year, were scraping the bottom of the barrel as their business strategies and relevance came under pressure.

However, 2023 might not bring good tidings as the discussion on margin and loss cost trends will likely inflect for the commercial players as discussed in our outlook.

Personal lines players would continue to reflect the benefit of earned rates, while reinsurance could come under pressure if the pricing rally fizzles out at the April or June renewals.

The note below looks at stock performance, valuation, and book value shifts over 2022:

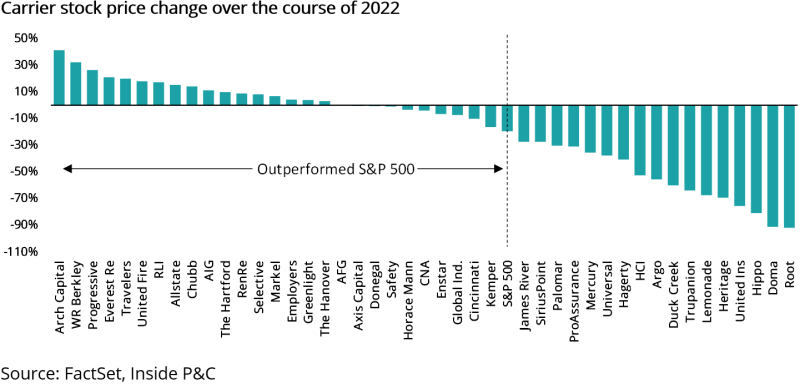

Despite volatility, insurance stocks generally outperformed the market in 2022

As we showed in a previous note, value stocks come into focus during uncertain times, and the past year certainly qualifies. However, this shift comes alongside a general market slip, which has resulted in high volatility as the market downturn has interacted with the move to safer stocks.

Given all the headwinds and the general performance of the stock market, it’s no surprise that most carriers are down. However, let’s look at these changes in context.

The chart below shows the 2022 stock price change for our IPC Select carriers and indicates which outperformed the S&P 500 performance over the same time period.

As seen above, using the S&P 500 as a benchmark, insurers have on the whole performed quite well, with several reinsurers and specialty carriers leading the pack.

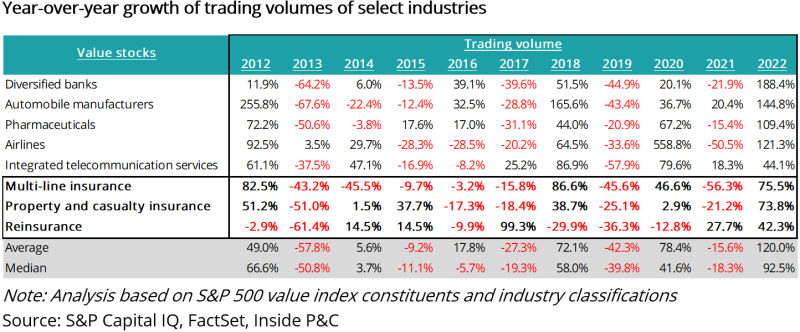

Another interesting factor to look at is the trading volume. The chart below shows the change in insurance trading volumes compared to several other major industries.

Note the change for 2022, which was the highest over the last ten years! If the Fed can tame inflation, and we get to an interest rate reversal cycle, value sectors could trend down over 2023.

With the Q4 earnings reporting season set to begin in a few weeks, we will get an early view of how the industry is positioning itself for 2023.

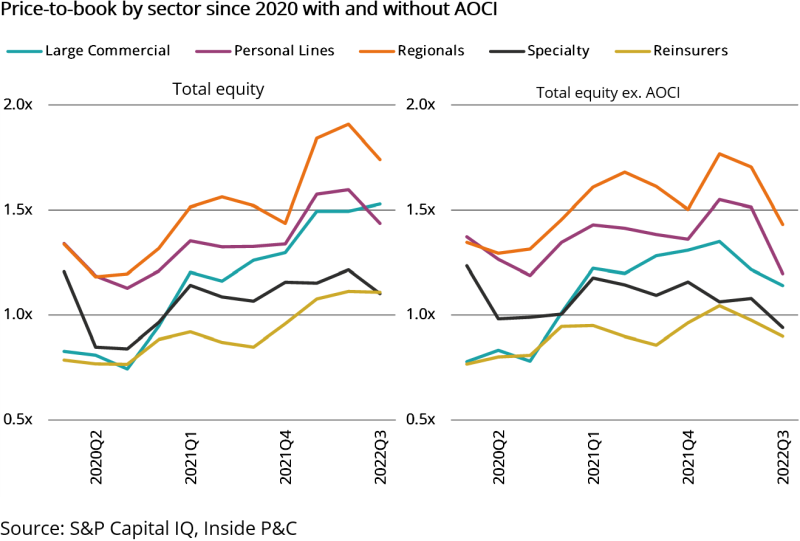

However, stock price movement only tells us a partial story. The moves relative to book value over time are even more important, as discussed below.

Price-to-book ratios have increased, but unrealized losses were the driver

The price-to-book multiple is a key metric for companies, and movement in the price-to-book over time is reflective of the company returns vs. its cost of capital.

However, this growth in the price-to-book ratio is only a true positive when the increase is due to an increase in the price. Because it is a ratio, a decrease in book value will also increase the multiple.

This isn’t commonly an industry-wide issue, but it becomes more relevant during times of economic stress and short-term shifts in the interest rates, as seen over 2022.

As we pointed out in our note on value creation, this past year and particularly the last few quarters, company book values have been impacted severely by unrealized losses.

While these aren’t actual losses at the moment, they factor into basic book value causing major drops and therefore causing the price-to-book multiples to go up.

In order to get a better picture of what is going on, we have repeated the analysis excluding accumulated-other-comprehensive-income (AOCI), where these losses are recorded, and placed it next to the original (left). This allows us to see the book values and resultant multiples without the noise caused by the downward revaluation of bond values.

In addition to the numbers being generally a bit lower (AOCI gains lowering the price-to-book), it is clear comparing the two side-by-side that the overall trend over the past year was also partially driven by the AOCI decreases (causing price-to-book to go up).

That said, since most insurers hold these investments to maturity, these negative marks on book value likely will reverse. However, this will take time, based on the current interest rate climate.

In addition, if the industry were materially impacted by capital-depleting events, these marks would matter and affect the industry’s ability to deploy capital.

Even excluding AOCI, positive changes were due to drop in book value

In the price-to-book charts, the trends were slightly different by sector, and the effect of removing AOCI produced different outcomes as well. This is because some sectors have been hit harder by the AOCI decreases (denominator), while others have been more affected by the stock market drops (numerator).

Again, taking a step back, insurers with the longest-dated instruments will generally have the biggest AOCI marks while shorter-duration industries will have the lowest marks.

Additionally, book value moves would also be the highest for industries or companies facing the toughest market climate or strategic challenges.

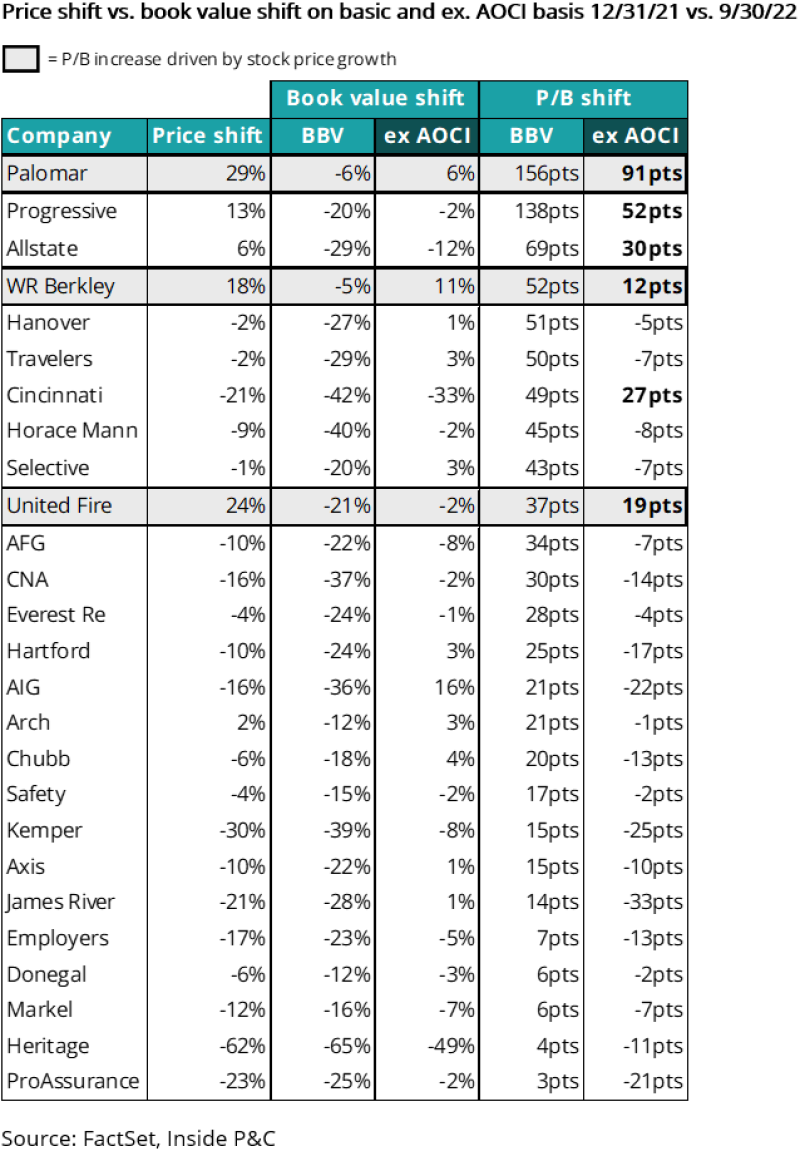

The chart above showed the ratios, so it isn't easy to distinguish which factors are affecting which carriers.

The chart below addresses this by showing the change in price compared to a change in total equity on both a basic book value (BBV) and an ex-AOCI basis.

Companies whose price-to-book ratio increased are highlighted based on whether the change was driven by book value or price. Note that only companies with an increase in P/B (on either basis) are included.

This analysis above paints a much clearer picture of what is going on. Of all the positive shifts, only three were due to an increase in stock price.

In summary, the tighter capital conditions made necessary by the Fed’s effort to combat inflation turned 2022 into an exercise in value investing. Industry and companies reported price-to-book ratios that looked materially better for 2022, but exclusion of the impact of AOCI reveals that, for most, price-to-book ratios fell. However, on a relative basis, insurance did outperform the S&P 500. For 2023, much will depend on the economic and loss cost inflation trajectory over the year.