It’s a constant balancing act.

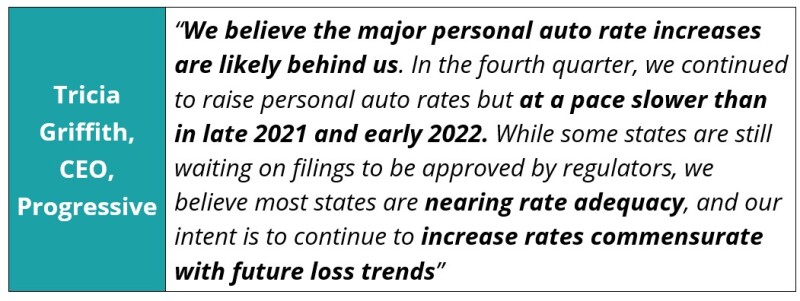

On Progressive’s fourth-quarter earnings call, CEO Tricia Griffith mentioned the idea of matching “rate to risk” several times. Furthermore, achieving proper “rate to risk” on a forward-looking basis, seems to be a key as to why long-term value creators like Progressive outpace competitors.

From the call, Griffith had this to say about Progressive’s auto rates:

She clearly understands, and more importantly, knows how to execute, rate positioning in anticipation of trends rather than having to play catch-up.

Below, we discuss the current climate in auto rates, the states undergoing the most change, and the overall effect that inflation is having on personal auto insurance premiums.

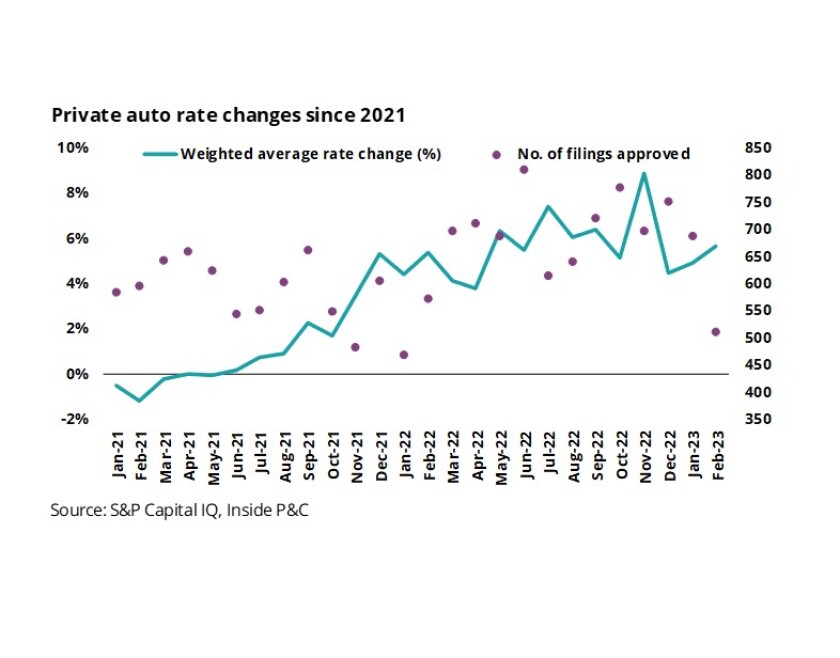

Firstly, P&C industry private auto rates have resumed their climb in 2023.

The lingering effects of the pandemic continue to impact US private auto insurers. Supply chain disruptions, rising inflation and economic pressure have posed new challenges for auto insurers. To compensate for these increasing loss costs and to improve performance, insurers continue to seek higher rates for their auto programs.

The Inside P&C Research Team analyzed rate filings approved in so far this year and found regulators across the US approved 650 private auto rate hikes for 68 insurance groups.

The chart below shows the weighted average rate change since 2021. We can see an uptick in rates again in the first two months of 2023, though the rate changes of 4.9% in January and 5.6% in February are lower than those we saw toward the end 2022.

These increases are driven by inflationary pressures, which we will discuss later in this note.

We dug further into the individual rate increases for carriers across different states to identify the biggest shifts. The chart below shows the 10 largest approvals by premium impact (excluding Auto Club Exchange’s 6.9% increase in California), along with the rate increase.

The top insurers that received significant rate increases during the period were State Farm, Progressive, Farmers, Allstate and Geico subsidiaries. State Farm’s 5.7% rate hike approved in Michigan on February 6 could be the most impactful and could lead to an additional $100mn in premium as the rate earns in.

Secondly, Georgia and Michigan had the largest increases, and California resumed approvals.

The rate filing approval depends heavily on state regulators’ rules and scrutiny. We looked at all states that signed off on key private auto rate hike requests and found Georgia and Michigan have approved the most significant aggregate rate changes year-to-date.

After a long pause, we also saw the California Department of Insurance start approving private auto rate increase requests in October 2022. In 2023, the state DOI approved six more rate increases, including one for Auto Club Exchange.

The charts below show the four states with the biggest shifts based on the aggregate premium affected. Each chart shows the top carrier aggregate changes since the beginning of the year, with both premium change and rate change shown.

It’s clear that rate increases aren’t particular to any region, but it does appear that, among carriers, some are still playing catch-up while others are far closer to rate adequacy.

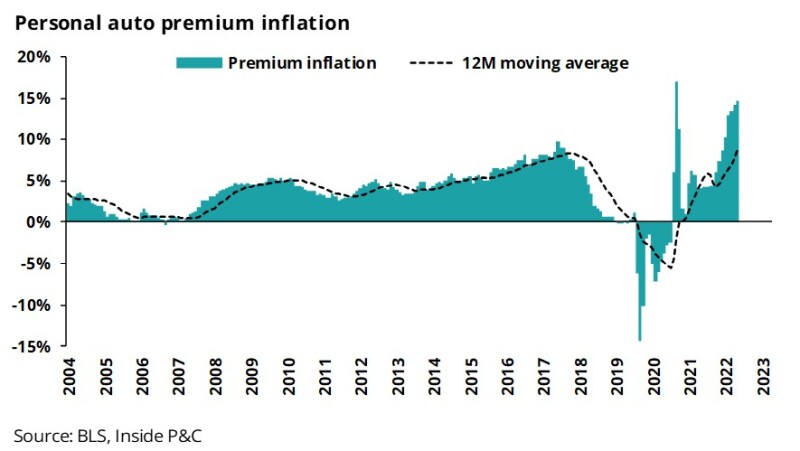

Lastly, double-digit auto premium inflation data shows increasing insurance costs.

The most discussed topic in the auto industry is rising premium costs for drivers. We analyzed January 2023 CPI data, which shows private auto premium inflation at 14.7% on a year on year basis. This is the second-largest spike in the decade, with the highest recorded in May 2021 at 16.9%.

The chart below shows premium inflation from 2004 through 2023, year-to-date. We can see a downward trend during the Covid lockdown due to less driving followed by an upward trend that has put us above pre-pandemic levels.

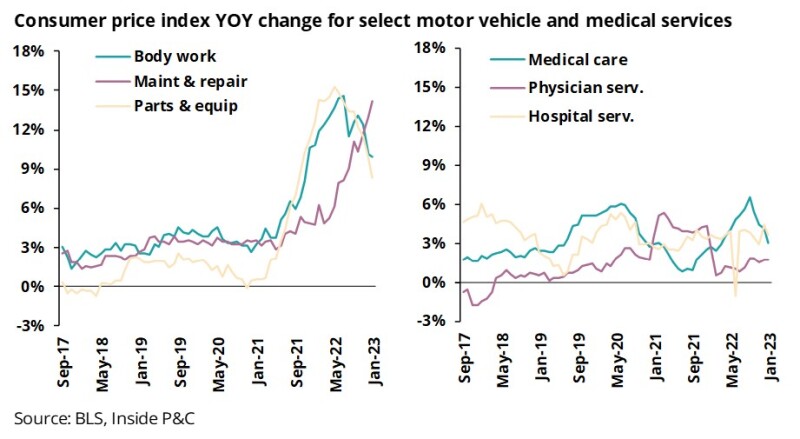

We’ve long heard about supply chain disruptions and increased vehicle maintenance costs post-Covid. In terms of auto industry loss costs, average year-on-year vehicle severity increase was at 10.8% led by bodywork, and parts & equipment costs, which increased by 9.9% and 8.3% respectively year on year. Maintenance and repair figures jumped 14.2% in January.

Medical CPI figures slightly improved as physician services remained flat in January 2023. Medical CPI numbers have remained stable and well below other loss cost factors affecting the industry. In addition, the used car prices were reduced by 12.8% in January year on year.

As shown in the chart above, the Manheim index which tracks used car prices dropped 12.8% on a year on year basis but saw an uptick in index values starting 2023.

So, while it appears that the most dramatic spikes to loss cost are behind us, we know that inflation is sticky, and the recent uptick in used cars is something to watch out for.

In summary, auto carriers are requesting as much rate as possible as they manage elevated loss-cost trends going into 2023. Timely and adequate rate action is key for auto insurers to achieve profitability in a competitive environment.