And in keeping with his Day 1 pronouncements to this publication, it is clear that we are not going to see a radical departure from Dan Glaser’s tenure. This is unsurprising given that Doyle has had a seat at the top table for seven years.

Instead, what we are seeing is the Doyle Evolution, with the emphasis firmly on perpetuating what has worked in his predecessor’s strategy and refining certain elements.

On the fourth quarter earnings call, Doyle defined the strategy as:

promoting a culture that attracts and retains top talent in the business;

investing to strengthen capabilities organically and inorganically;

positioning the firm in segments and geographies with attractive fundamentals;

leveraging data and insights to help clients become more resilient and find new opportunities and

delivering Marsh McLennan's full value proposition to enable client success.

Points 1-4 could easily have been articulated in the Glaser era. Doyle’s key addition is (5). It references a program understood to be underway at Marsh McLennan – known internally as Ready – to enhance collaboration, which the firm expects to drive both revenue growth and margin expansion.

The program can trace its roots back a couple of years, with work to break down internal siloes and knit the firm more clearly together as one enterprise already underway before. Ready itself has been in genesis since around the middle of last year.

Ready embodies a view about how Marsh McLennan sets up its culture, organizes itself and goes to market, but the decision to take this tack also says something about the borders of the group.

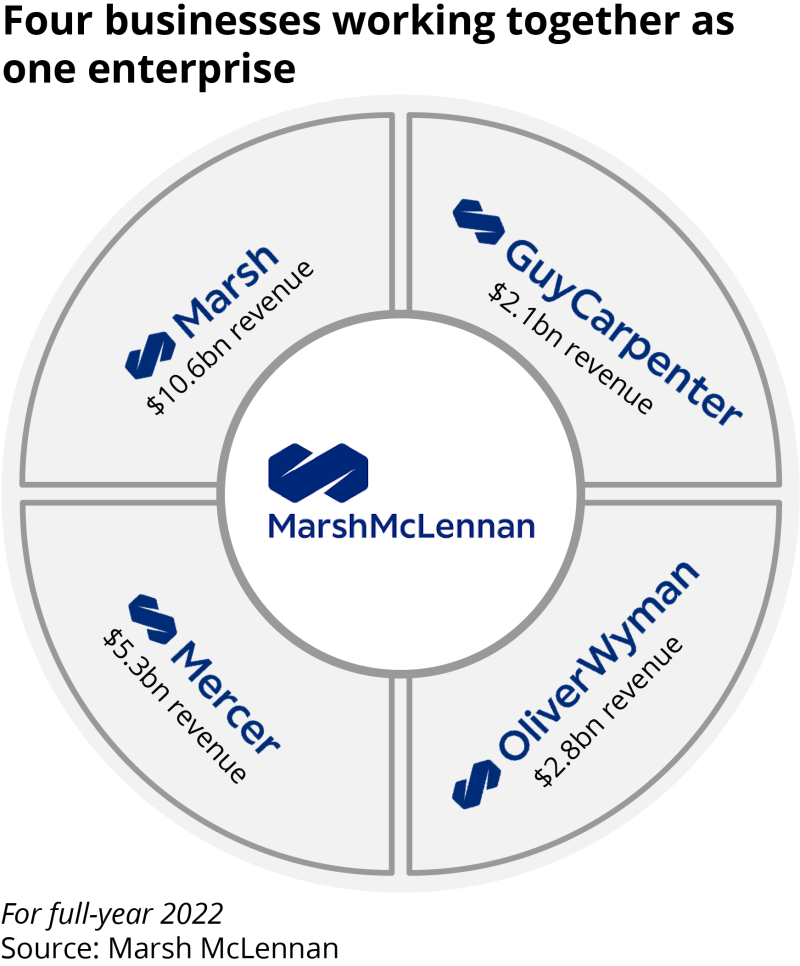

Given its ownership of Oliver Wyman and Guy Carpenter, Marsh McLennan is a broader business than both Aon and WTW. Having looked at the group with fresh eyes, Doyle has judged that Marsh McLennan can deliver more based on this breadth than it loses from the increased complexity, as well as the lower margins and higher cyclicality of some of its businesses.

Doyle has also implicitly reaffirmed what we previously called the Glaser Guarantee – that adjusted operating margins would rise every year. Although only explicitly stated for 2023 (Marsh McLennan doesn’t provide guidance beyond 12 months), it seems likely that this will be a rolling target.

Continuity is also retained around capital allocation priorities, with M&A perceived as a better long-term lever for creating value than share buybacks, although 2022 was a highly active year for the latter.

While the firm intoned $4bn of capital resources on the call, the real number is more like $20bn for the right opportunity given available leverage, with the group of US PE-backed mid-market brokers likely to be the targets of choice.

Besides throwing the full capital resources of the group behind the home run that has been MMA, the MGA business is likely to be an area for investment. M&A may come into play, but sources have also suggested that Marsh McLennan will seek to use this as its true small commercial play.

A large play in wholesale, through an acquisition of one of the Big Three, is believed to have been ruled out, but a small foray to target business in this same small commercial segment is also thought to be under contemplation.

Here’s a quick summary of the notable elements of the strategy beyond the inevitable things like talent acquisition and use of data/analytics.

Ready:

A starting conviction that Marsh McLennan is more than the sum of its parts, and benefits from being a broader business than competitors

Collaboration across the brands to deliver a broader range of solutions to clients to drive growth

Work to simplify and streamline the group to eliminate duplication between brands and boost margins

Expense discipline:

The firm has recommitted to continuing to raise margins, implicitly every year

Doyle took out headcount early on alongside other cost saves, demonstrating edge that will appeal to investors, but with potential cultural challenges

Growth opportunities:

The leadership favors M&A over share buybacks, and could stretch to $20bn if it re-levered

A PE-backed US retailer in the $500mn-$1bn Ebitda range makes most sense as a target

MGAs will also be a growth focus, with the firm looking for ways to target small commercial

Targeting small commercial may also include a limited foray into wholesale

Let’s take each of those areas and look at them in more depth.

A Ready: The opportunities at the intersections

As suggested in a big piece from August last year anticipating the CEO succession, one of the key strategic issues that Doyle would face was more decisively answering the question about whether Marsh McLennan is one operating company, or four companies sitting under a holdco. (For background see: “Marsh McLennan: The last decade and the next one”)

Doyle has clearly come down on the side of a more integrated culture, operating model and go-to-market strategy.

Crucially, it is an attempt to leverage the benefits of the breadth of capabilities and solutions in the group. Which is to say, it makes a virtue of each of the four units including consultancy Oliver Wyman, which looks a little different than the other three.

Oliver Wyman is a fundamentally lower margin business due to the remuneration structure of its partners and is more cyclical than the other units. It also engages directly with the C-suite, and creates content on key themes/industries that can be utilized by the rest of Marsh McLennan. It is also different because it is a challenger to the likes of McKinsey, BCG and Bain – where Marsh, Mercer and Guy Carpenter are among the dominant players where they operate.

At a high level, the program is an attempt to offer a broader range of services to clients, reflecting the increased complexity of client needs, and the untapped advantages of leveraging a broader range of capabilities, which are often already looking to address the same macro issues.

The second layer is an attempt to simplify and streamline the Marsh McLennan machine, reducing cost, supporting cross-sell and easing some of the large company pains of an organization that is at times hard to navigate.

All told, it is expected to help generate growth Alpha, and to fuel margin expansion.

Leadership changes have already been made, with some senior leaders in the business including Flavio Piccolomini and Chris Lay given Marsh McLennan roles and charged with accelerating collaboration and eliminating duplication.

It is understood that nine areas have been identified for growth, with some believed to be centered on industries, and individual leaders targeted on hitting revenue numbers. A parallel leadership and target structure is understood to exist for cost savings related to the project.

The strategy seems to be broadly known, but some of the details are not – partly because of the automatic read-across from Aon United, which it resembles but also differs from.

Important differences include Marsh McLennan’s commitment to retaining its individual brands, its resistance to a single P&L for the group, and its decision not to have a single client executive acting as the gateway to all its services. It is also an internal program name – rather than something it presents directly to clients and investors.

Making the most of Ready will crucially rely on working out where it makes sense to collaborate to deliver for clients, and where collaboration is being pursued for its own end or in the service of company politics.

In that vein, to make it work, clients must be offered something that truly adds value, rather than a lazy cross sell, and the work must reach high enough in the organization to unlock the opportunity. The risk manager can’t unlock the pension advisory mandate. Much of this turns therefore on Oliver Wyman as the unit with the best C-suite access.

B. Doyle discipline: Margin expansion every year

In his section in strategy on the call, Doyle emphasized the firm’s “track record of execution and financial performance” and committed that these would remain areas of focus.

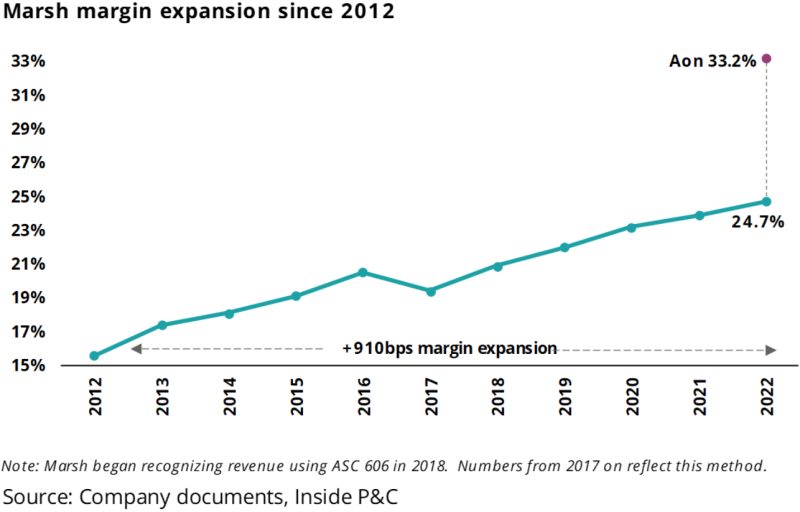

Although the firm probably made the strongest case I have seen for an environment that continues to be supportive of growth at brokers, increasingly it seems likely that the focus in broking will be on expense discipline.

Glaser had an effective commitment in place to deliver an expansion in adjusted operating margins every year, and this seems to implicitly remain in place.

Doyle has already given an early answer to the questions some asked about whether he had the edge his predecessor had shown

As a broking firm, it has a lot of levers to pull if it comes under pressure, including reducing its bonus pool, and dialing down T&E.

Doyle has already given an early answer to the questions some asked about whether he had the edge which his predecessor had shown, by cutting jobs alongside his first earnings call.

The firm took a $233mn restructuring charge driven by a relatively even mix of “workforce actions”, rationalizing technology and reducing its real estate footprint.

Savings that will drop to the bottom line in 2023 are expected to total $125mn-$150mn (~70 bps on margins), with further cost savings projected in 2023 and 2024. Typically, though, Marsh McLennan is conservative, and you would expect it to outperform the stated target.

This kind of line of sight on cost savings is likely to please analysts and will be necessary if Marsh McLennan is going to deliver double-digit adjusted EPS growth going forward, as market organic growth trends back to mid-single-digits.

Margins is one of the areas where the Aon comparison hurts Marsh McLennan, with the former having a ~850 bps margin advantage. Some of this Aon’s greater efficiency – but a fair amount of it is business mix, with Aon lacking a lower margin management consultancy business and having a larger weighting to higher margin reinsurance broking.

While it will find favor with investors, it is likely to be somewhat culturally challenging internally as Doyle starts his tenure with job cuts.

C. Growth opportunities: Looking for a $20bn bet

Public pronouncements on M&A from firms have relatively little value, given the need for freedom of maneuver and secrecy to operate effectively in this area.

On its call, Marsh McLennan at least made clear (in the words of CFO Mark McGivney) that “we favor attractive acquisitions over share repurchases and believe they are the better value creator over the longer term”.

However, the firm continues to point to $4bn of likely capital deployment across M&A, share buybacks and dividends – suggesting only a couple of billion available acquisitions.

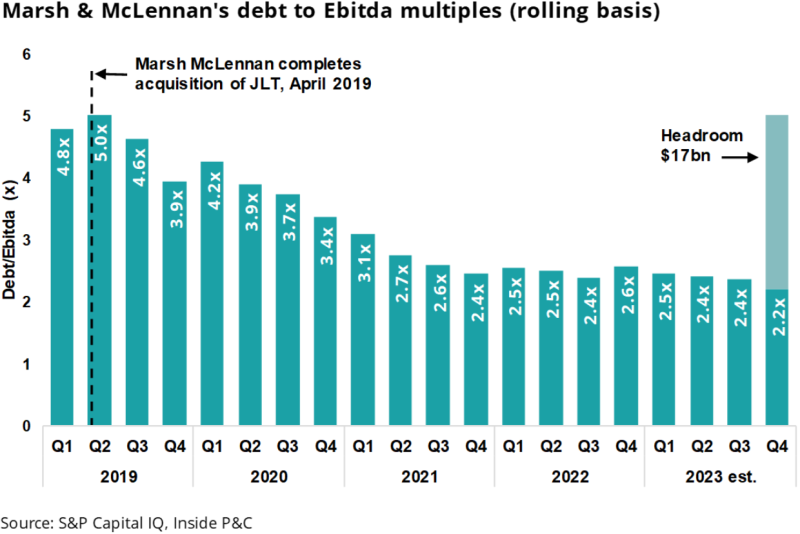

The reality is that by re-levering and using the free cashflow not earmarked for dividends, Marsh McLennan can stretch to a ~$20bn deal without issuing equity. Where Doyle chooses to train this firepower will to a large degree define his tenure as CEO.

JLT completed in April 2019 and has been fully digested, and with the CEO handover now complete, both major obstacles to a fresh deal at scale have been passed.

The likeliest target for the business is a PE-backed US retail brokerage, with ~$2.5bn-revenue mid-market platform MMA as the acquiring entity. Timing may be favorable, with evidence that platform multiples are coming under some pressure, and deals that bring a full change of control essentially stalled.

There are also a range of platforms with the scale to meaningfully move the dial, with Ebitda in the $500mn-$1bn range, roughly equating to $8bn-$18bn of enterprise value.

To minimize risk around talent flight and to be able to realize synergies, it is likely that a truly integrated business would need to be bought – with a full integration with MMA pursued. Although the whole market is now preaching the gospel of integration, the real state of these businesses means that this would narrow the field substantially.

Lots of things could stay Doyle’s hand.

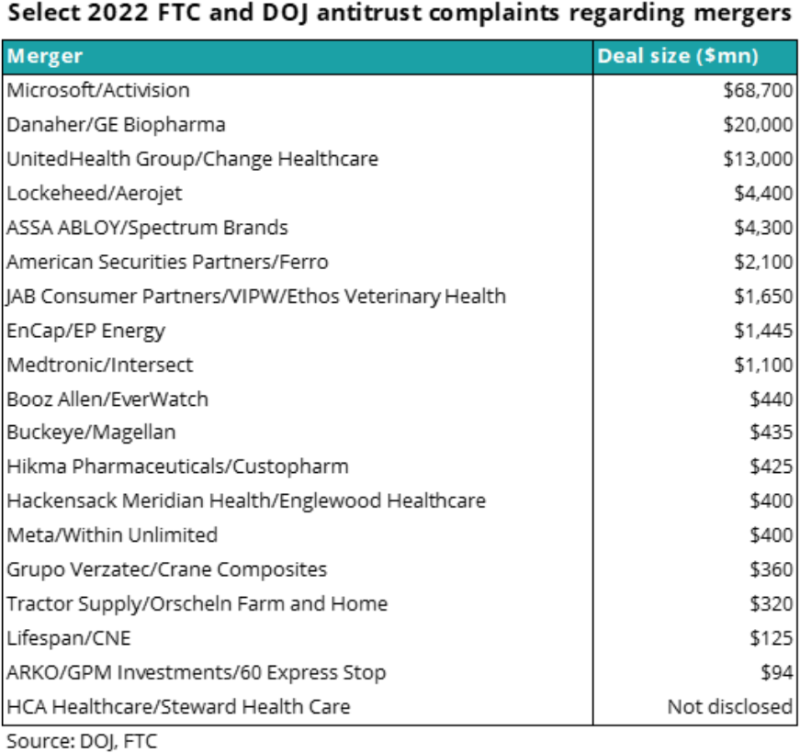

The antitrust landscape is terrifying for large corporates right now, even with deals that clearly aren’t anti-competitive. Waiting out Lina Khan at the FTC would reduce risk. Equity or debt markets could upset any deal, particularly if there is a recession. And personnel issues can be intractable in businesses where successful CEOs that manage to keep their firms private another three-to-five years can hope to make nine-figure sums.

All that said, there is an opportunity cost to waiting.

Just as a big deal for MMA would give Marsh McLennan more penetration in the US mid-market, as it looks to build out away from its large corporate heartland, the firm is interested in further penetrating small commercial.

This is believed to have been identified as a target growth area, with the US MGA business Victor one way of seeking to increase share.

It is understood that early-stage work is in train to invest to build a digital storefront for the thousands of agents that trade with the MGA to improve ease of access.

Marsh McLennan’s M&A activity in the MGA space has been curbed by the runaway multiples in recent years and the need to prioritize capital allocation to MMA. But this could be an area where it looks to become more active as well.

In a prior piece, I floated the possibility that Marsh McLennan would look to get back into wholesale as a means of playing the structural growth in E&S and closing off leakage.

A major deal to take out Amwins, Ryan Specialty or CRC is believed to be off the table (the revenue dis-synergies would be horrible), but a smaller foray into wholesale broking as another means of playing in the small commercial space is possible.