The high-net-worth (HNW) homeowners’ space is in its “hardest market in decades”, sources have told Inside P&C, as carriers retrench capacity and rates continue to accelerate with double-digit growth.

Further, the popular opinion is that the hardening will continue for the next two to three years until carriers figure out a way to better combat the volatility in their losses, or rates harden enough to beckon capital back to the market.

For rate, carriers are pursuing 8%-12% increases for non-cat accounts in admitted markets, sources said, which compares to roughly 6%-8% rate increases last year.

However, the regulatory limitations put on rates in the admitted market is putting the squeeze on carriers, with reinsurance costs soaring.

In search for freedom of rate and form, carriers have been migrating to the non-admitted market. Here, sources have pointed to a wide range of rate increases in the E&S space this year starting from 20%, up to “easily above 150%” for wildfire, wind-prone areas.

One broker source said the portion of clients’ HNW homeowners’ business placed in the non-admitted market has grown from mid-single digits to closer to 30% over the past 18 months.

HNW writers have seen a challenging loss environment, with inflation pushing up claims volatility and secondary peril losses hurting the market.

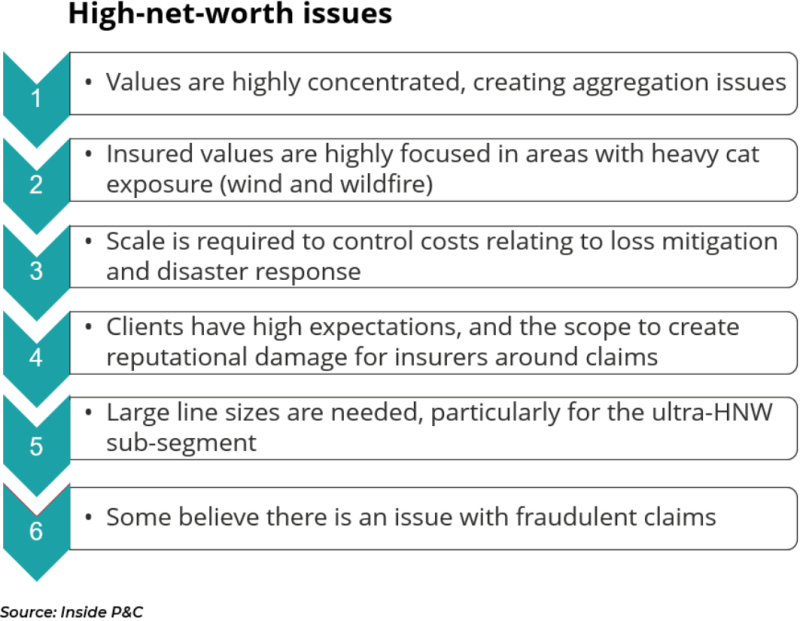

The clustering of exposures in a handful of wealthy areas generates significant aggregation risk, which is extremely hard to manage on a single balance sheet, and is capital consumptive. Top-three writer AIG's recent deal with StonePoint to spin out its $1.4bn-premium US high-net-worth insurance out as an MGA underlines the challenges the space is facing.

It is difficult to assess the performance of the overall market, as it isn’t broken out as a statutory line, although market leader Chubb is making money in North American personal lines. However, capacity has exited the space as carriers attempt to right-size exposures.

In the E&S market, there is a stark mismatch of supply and demand, especially in peak loss zones like California and Florida.

In these states, most new accounts are already being written a non-admitted basis and yet, clients “might not even be able to get a price for anything,” one broker said.

That is a difficult pill to swallow for insureds and their brokers, who for decades were used to navigating a “sleepy market” where one carrier typically took on the full limit of a single account.

Over the past year and a half, that trend has changed in a way where the lead carrier would put up only a fraction of the total limit, at around 10%-30%, sources estimated. On the whole, line sizes are down.

Programs are still managing to get placed, but one broker noted there had been recent cases where insureds had had to accept lower limits if the insured values were in the tens of millions of dollars.

“It's not the market that we had even five years ago where we had three insurance companies competing on [one] business,” another source added. “Now, if you're in a high-risk area, we're thankful if we can get one solid offer.”

Among HNW writers, Chubb, AIG and Pure Insurance continue to hail as the top three players in the space, followed by firms including Vault, Cincinnati Insurance and Berkley One.

Homeowners’ business accounts for roughly 60% of the US HNW market or more, according to sources. That has tied it to move in a similar fashion to the cat property market.

“Bad weather and natural disasters have disproportionately found themselves to be in areas where wealthy people live […] So since 2017, for the first time in a long time, the high net worth underperformed compared to the other [property market],” one HNW carrier executive said.

Another source noted that the impact of weather events and record-high inflation hit the HNW market after a historical increase of wealth and a building boom. According to a Vault study, the number of US households with a net worth more than $1mn increased by a compound rate of 5.3% between 2009 and 2019, while total US households increased by only 0.9% during the same period.

Like commercial property, HNW homeowners’ insurers also struggle with inflation and rising reinsurance prices that aggravate losses occurred by weather events.

Given that HNW business involves costlier materials and skilled craftsmen, carriers in the space have generally been better at staying on top of valuation updates compared to commercial property insurers, according to sources.

Nonetheless, inflation over the past year has been such that annual inflation adjustment factors have doubled. Price hikes on consumer goods and supply-chain bottlenecks have also aggravated additional living expenses (ALE), which include the rent that HNW carriers provide to clients during reconstruction.

Historically, the annual inflation adjustment factor in high net worth was around 6%-8%, one broker suggested, adding that range is being reset at 12%-15%.

Despite this, deductibles in the HNW space have remained “traditionally low” and at fixed dollar amounts, some sources say.

“You'd be surprised how many people with money keep the $1,000 deductible – it's mind blowing,” one broker said.

A HNW carrier executive noted that insurers have just started to introduce percentage deductibles, which is already pretty much widespread among commercial property underwriters that impose deductibles of 2%-5% to property value.

“It'll have the effect of raising the deductible and scaling it for inflation,” the source added.

Water, not wind

Terms and conditions are being revisited as well, as insurers seek to reduce exposure to natural perils.

Carriers are paying particular attention to keeping water damage in check, the number-one loss driver In the HNW homeowners’ segment. In the standard property market, water losses are sub-limited, one source said, whereas in the HNW space, it isn’t.

Pure, for example, saw 55% of its reported homeowners’ losses come from water damage in 2021, when Hurricane Ida and Winter Storm Uri hit. Fire followed second that year with 17% and wind, third, at 13%.

Sources say that HNW homes are often built better to withstand wind, especially newer ones that are constructed under the latest building codes. But water is more intrusive - whether it’s storms entering through broken roofs and windows, or pipe bursts, which are increasingly becoming a problem in old cities like New York.

Water also creates mold on expensive housing materials or damage content saved indoors like artwork, which in some cases outweigh the value of the structure that holds them.

One emerging trend is a stronger push from insurance companies to make clients install automatic water shut-off devices. They can detect water flow or leaks in the household, start an alarm and shut down the water line.

One carrier source anecdotally provided an instance of a water damage case where the loss could have been one-tenth that size if a water shut-down device was activated.

Flood is typically not included in HNW homeowners’ policies unless the client purchases excess coverage. Nonetheless, sources have pointed to an ambiguity where carriers may end up paying out for wind-driven rain, versus damage from risen waters.

“The language around what is the peril needs to be clarified so that we all can objectively agree [on] what is covered and what is not covered,” said another insurer executive.