The lack of meaningful catastrophe activity in Q4 2023, despite another active year for losses overall, means that results would likely be favorable vs. prior quarters. This in theory allows the industry to kitchen-sink this quarter to get ahead of any future development and build an additional reserve buffer for prior years.

The flip side to this argument is that any kitchen-sinking could create short-term pressure on the stocks, which had already underperformed S&P for 2023.

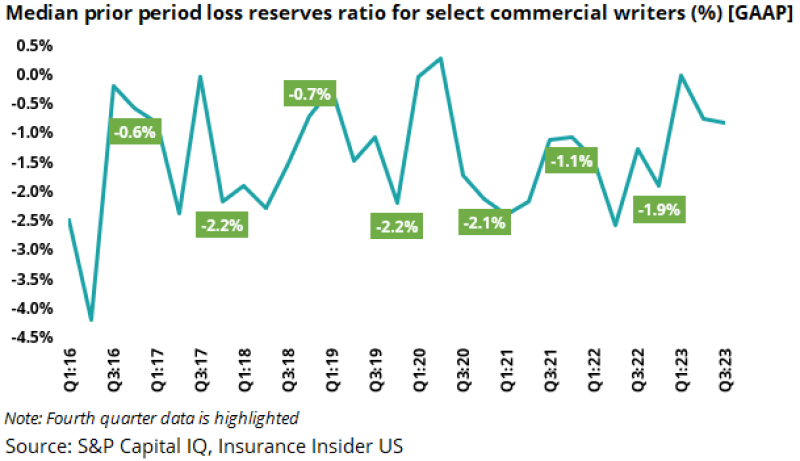

The chart below shows prior-period releases for the select group of companies in the commercial lines space, with the fourth quarter releases highlighted. Noticeably, the fourth-quarter releases are higher than the other periods for many periods.

This makes intuitive sense since the fourth quarter often includes the results for the year-end, which requires deeper reserve review processes. Hence, we would not be surprised if some companies use this quarter as an occasion to take some early bitter medicine of reserve adjustments.

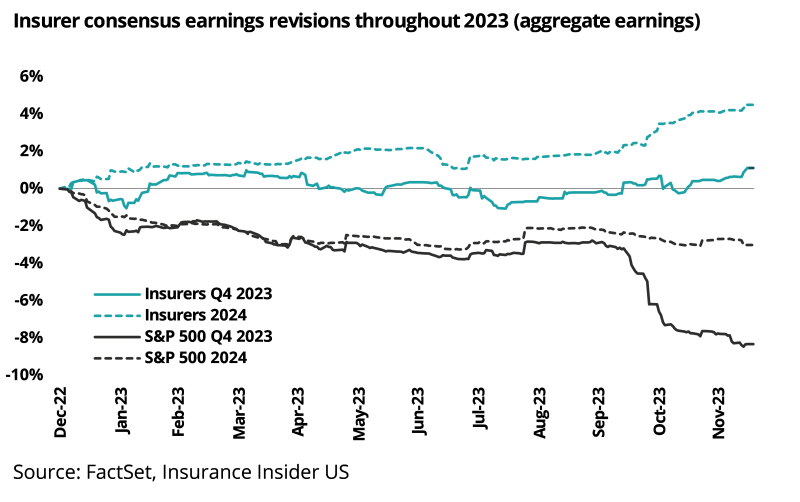

However, street estimates for Q4 2023 shown below seem to be on a slight positive trajectory reflective of a quieter catastrophe quarter. This does set the space up for a negative surprise if companies take any reserve clean-ups this quarter.

The calendar below shows the schedule of earnings reports for Q4, with Truist and Travelers leading the charge and setting the stage for early trends.

In general, the major themes we expect by sector are:

Commercial lines:

Expect renewed discussion on AY 2015-2019 loss reserves and how companies view their loss picks. Beyond that, the focus will be on the usual topics of social inflation, rate increases and the economy's overall direction.

Personal lines:

Will this be the quarter? If Progressive’s monthly results are a proxy, this quarter could be the one where we finally start putting the noise in the rear-view mirror. On the homeowners’ side, expect discussion on trends and by-state actions. Beyond that, the results could be better since loss activity has been on the lower side.

InsurTech:

Whack-a-mole continues with companies balancing growth vs. capital vs. loss trends. Since short interest remains high, expect volatile stock reactions on earnings.

Reinsurance:

Although the January 1 renewal was strong, it was likely below initial expectations. Similar to commercial, expect questions on casualty reinsurance reserve adequacy. We expect a good earnings season on a quarterly results front, due to a lack of large loss activity.

Florida:

We expect continued discussion on new entrants in the marketplace and the overall health of the sector. Results should be strong due to low regional losses.

Brokers:

As the first derivative, expect questions on the longevity of the cycle. Also, expect detailed discussions on where we go from here during this soft economic landing. Organic growth numbers should be good, although they could show a downward trajectory.

We expand on these ideas below.

Commercial:

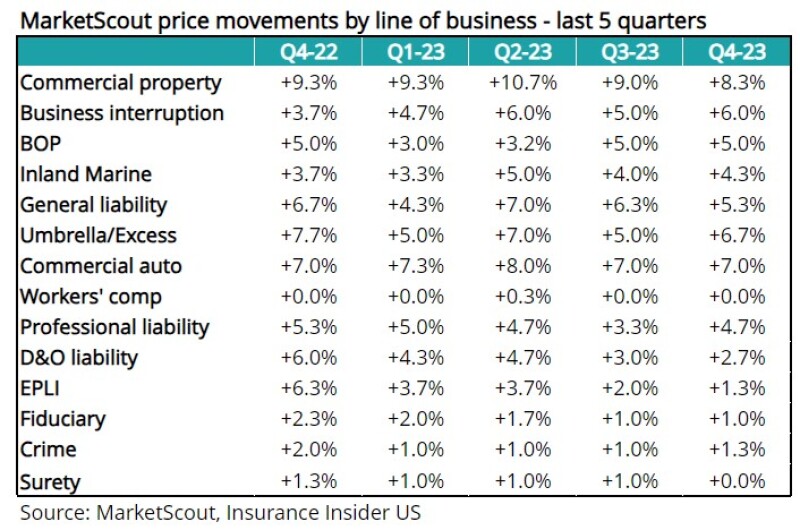

Recent pricing data shows a continuation of trends seen in prior quarters with sporadic sequential declines, which are unsurprising. However, the focus should be on these pricing numbers translating into earnings and ROE growth.

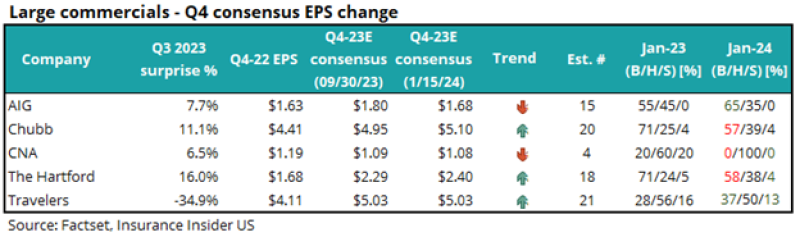

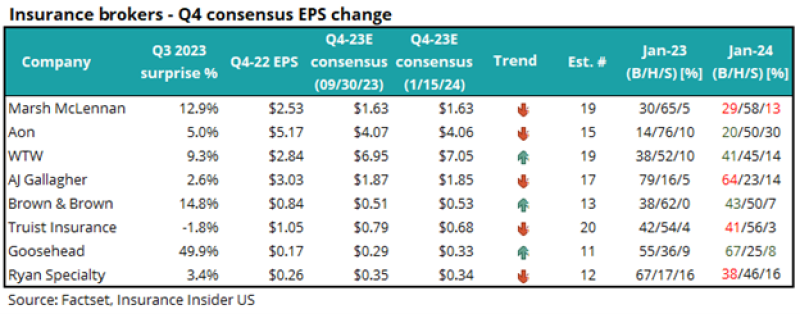

The chart below shows projected earnings per share for the fourth quarter as of this week, and also looks at the same number 100 days or so ago. It’s a mixed bag when looking at the cohort. We have added two columns this quarter to show the street sentiment, which compares the % of analysts who had a call for buy/hold/sell on the stock. This reveals an overall negative bias vs a year ago.

We have added charts in this preview showing the median reserve development for the group. As shown below, the fourth quarter often seems to be a period of reserve releases, which goes back to our point that we would not be surprised if companies took the opportunity to take reserve action.

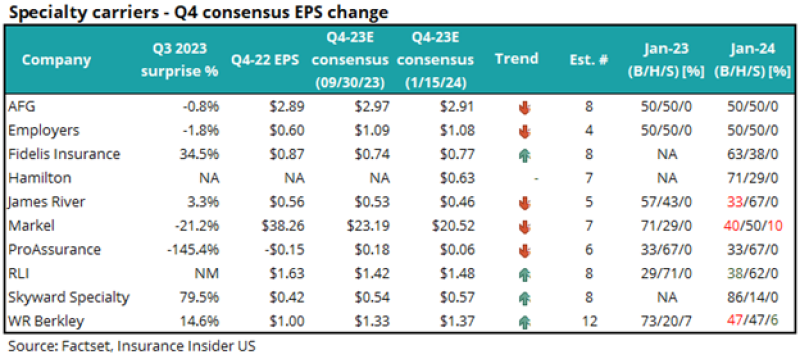

The specialty sector below shows a similar trend with half of the street estimates moving up.

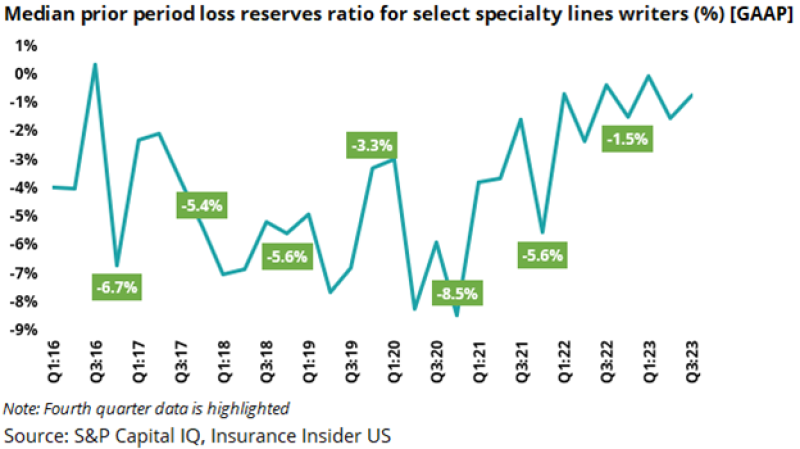

Like commercial players, the chart below shows median reserve releases for the specialty players. Clearly, specialty players have better-managed reserves, resulting in higher releases over time. We anticipate a lower level of reserve volatility in this sub-segment.

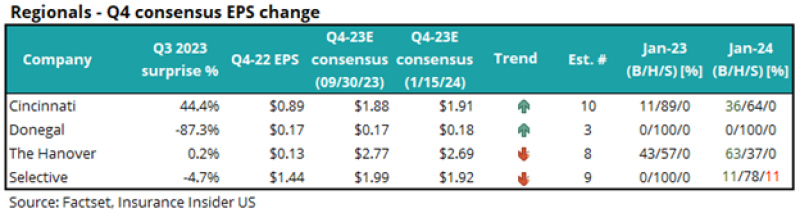

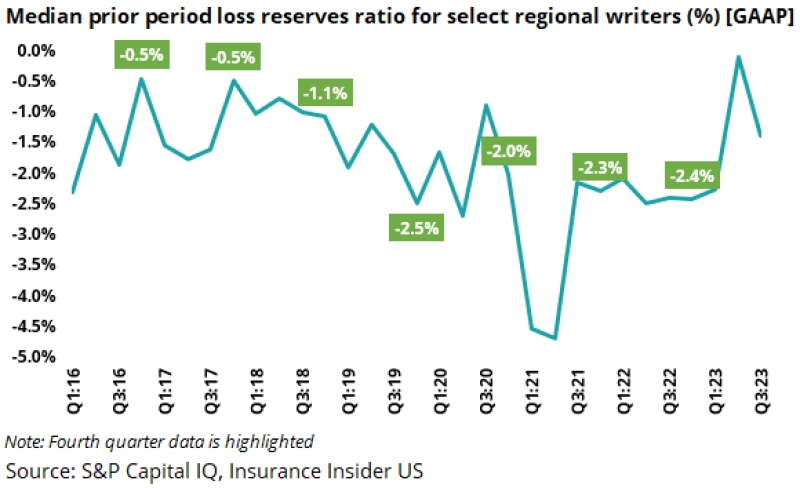

A similar mixed trend is anticipated to play out in the regional space, although we would note the positive bias in the ratings for 2024 vs. 2023.

An interesting trend is visible when looking at the median releases over time. These seem to have picked up as regionals have demonstrably improved their quality of books. We anticipate a lower level of house-cleaning in this space.

Reinsurance:

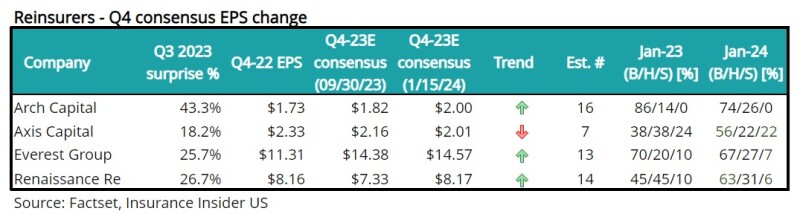

Reinsurers’ earnings have mostly been revised upwards since the end of the third quarter, reflecting lower-than-expected catastrophe losses. Recent broker reports have pointed to a good, albeit slightly disappointing 1/1 renewals. We expect conference calls to focus on April 1 and July 1 renewals and the available capital level.

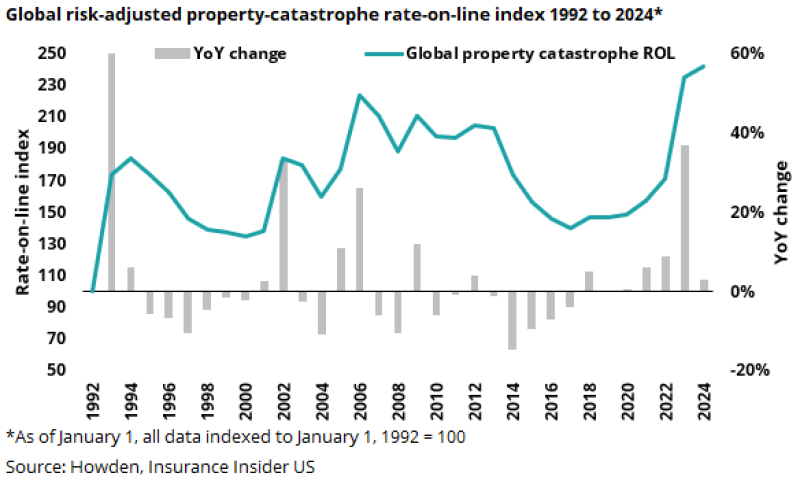

The chart below shows the ROL, which is modestly up vs. the prior year and still at all-time highs.

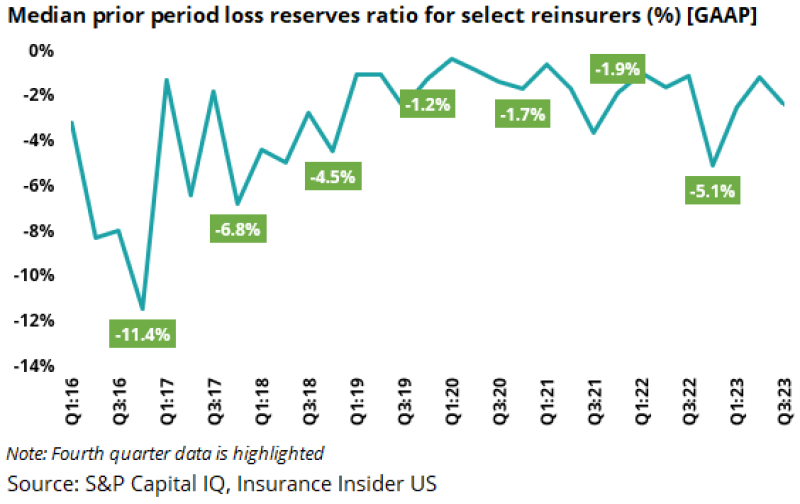

Beyond rates and catastrophes, reserve adjustments are the topics we anticipate getting more color on during earnings and conference calls. Historically, this group has benefited from a larger level of releases. Additionally, with the pivot to a balanced book of business encompassing insurance and reinsurance, some companies might also consider reserve adjustments for their insurance writings during the quarter.

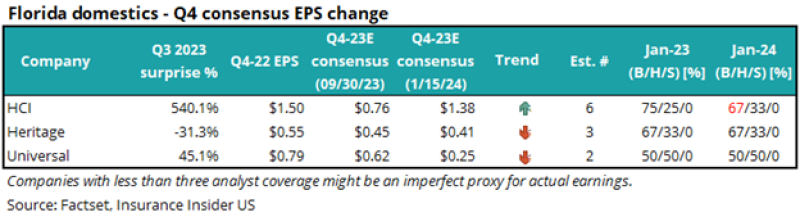

Florida domestics:

This group has had a relatively good year due to a lack of defining hurricane losses vs. past years. We can see this in the shift in HCI’s earnings estimates over the past 90 days or so.

We expect conference call commentary to focus on the impact of new entrants, including reciprocals.

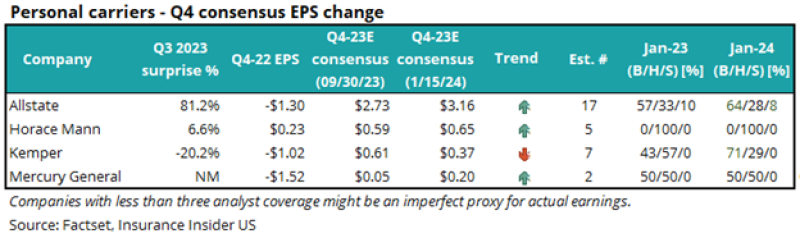

Personal lines:

Although most of 2023 was rockier for multiple franchises, it is beginning to feel like we are seeing the light at the end of the tunnel. The estimate summary confirms this, apart from Kemper, which continues to address franchise-level challenges.

Personal Auto

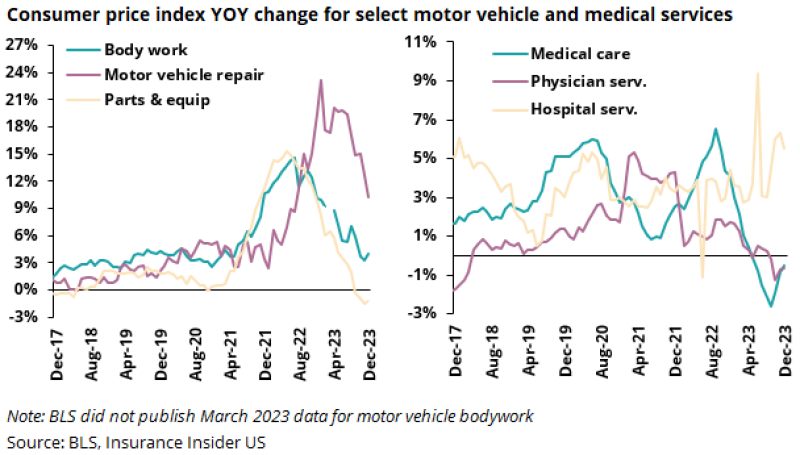

Last week, the latest BLS/CPI data confirmed the continuing moderation of several severity-related items, as shown below, and we expect conference call commentary to reinforce this.

The rest of the year will focus on state-level actions and rate action needed to widen the gap between pricing and loss costs.

Homeowners’

As discussed in our outlook, the homeowners’ sector has seen similar underwriting actions, including state-level exits and pullbacks. The bigger challenge remains the elevated level of losses including from SCS, that we have seen in recent years. Consequently, we anticipate greater scrutiny from investors for this line of business.

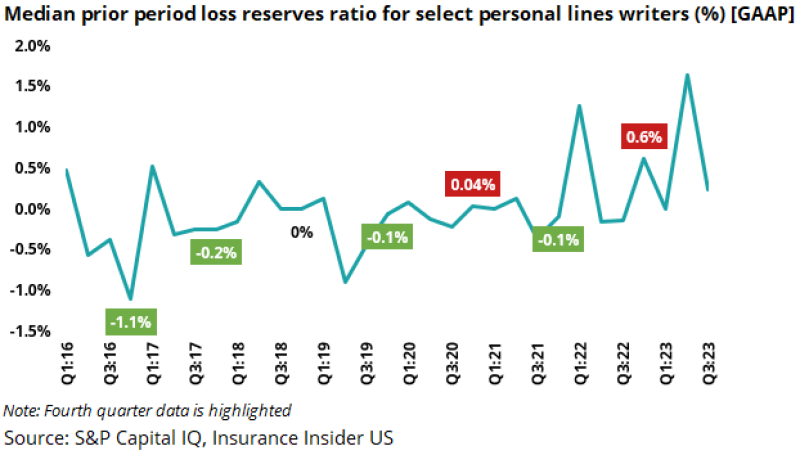

The chart below shows the median reserve releases on a quarterly basis. Note the adverse development shown in red vs. other sectors shown above. The adverse development has trended down as noise from personal auto prior period normalizes. We expect this quarter to have a lower level of adverse development.

Brokers:

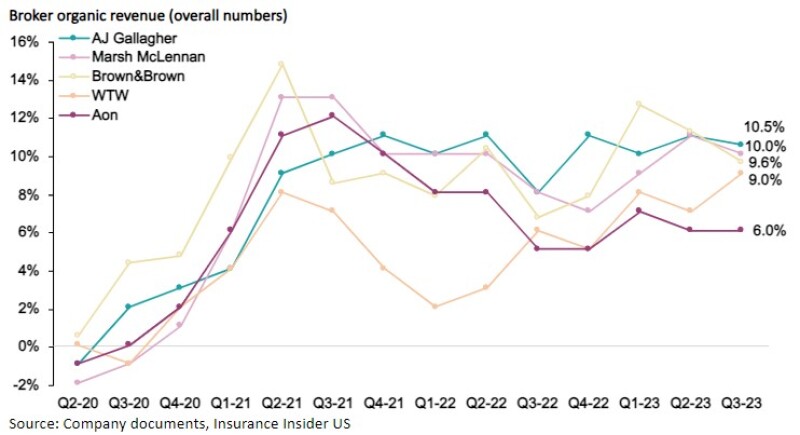

As the leading indicators, brokers find themselves at an interesting point in the insurance cycle. They have demonstrated meaningful organic growth and margin expansion, but these have begun to taper off.

Suppose commercial writers start discussing prior-period reserve clean-ups and a consequent slowdown in their top lines. Will brokers be able to disconnect from the overarching discussion and continue to project strong organic growth?

On an aggregate basis, overall earnings expectations have remained flat while S&P had trended down.

On a company basis, the estimates show a 50/50 split with modest tweaks in either direction.

We have been previously surprised on the upside on when the broker super-cycle will come to an end after a Q1 2023 resurgence, but recent quarters do point to an orderly climbdown.

In summary, the fourth quarter does present the opportunity for commercial-predominant writers to kitchen sink their reserves and get ahead of the potential for future reserve adjustments for AY 2015-2019. If we don’t see any reserve adjustments, this space should have a good quarter due to the lack of large loss activity.

On the personal lines side, auto might finally reflect the light at the end of the tunnel while homeowners’ will reflect continued corrective action. Results will again benefit from a lack of large SCS and other non-cat activity in the fourth quarter.

Although quarterly results will be strong for reinsurers, the focus will be on future rate expectations and any reserve cleanups for hybrids.

Broker results will reflect the usual tightrope between broader economic conditions and managing expectations of a slow climbdown from peak organic growth rates.