Personal E&S

-

Economic volatility, including from tariffs and rising interest rates, is reshaping risk profiles for specialty insurers.

Economic volatility, including from tariffs and rising interest rates, is reshaping risk profiles for specialty insurers. -

California, Florida and Texas all saw decreases in monthly premium growth.

-

The company plans to launch in New York and New Jersey next year.

-

This is up from the $300mn in capacity the MGA secured in 2024.

-

The transition will be implemented starting October 15.

-

The standard market has not ‘meaningfully’ impacted the rate of flow in the aggregate.

-

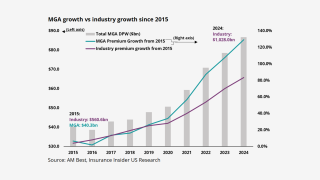

MGA growth is still strong but has passed its 2022 peak.

-

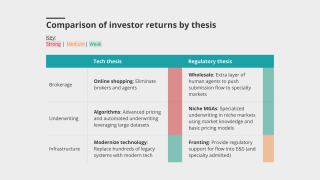

The business will divide into US wholesale and specialty, and programmes and solutions.

-

The carrier has received 12,300 claims as of 28 March.

-

Surplus lines are still strong, but not the standout they used to be.

-

Shift to growth includes all geographies in which the company does business.

-

Insurers and distributors must adapt or risk irrelevance.

-

The MGA will have a broad casualty-focused appetite with Lloyd’s capacity backing.

-

The total includes fire and smoke damage plus living expenses for evacuees.

-

Most carriers paid more in homeowners’ claims than they collected in premiums.

-

The carrier is the largest writer of homeowners’ multi-peril in the state.

-

As fires still rage, many fear early $10bn-$20bn estimates were too optimistic.

-

This could see it surpass the 2017 Camp Fire, which cost around $12.2bn.

-

Management is showcasing its ambition, but it’s also dialing up risk.

-

Idaho and Minnesota far outpaced other reporting states in premium growth, stamping office data shows.

-

Insurance Insider US chats with Kevin Doyle on the state of the E&S market during WSIA.