This past weekend, we managed to catch the sequel to the 2009 movie. The Way of Water expanded on the 2009 themes with an additional thread on family. It was worth a watch as sequels go, despite difficulty tracking all the characters and their subplots.

However, unlike Avatar’s sequel, the P&C industry follow-through from 2022 into 2023 could be less favorable than anticipated. For 2022, the P&C industry managed to achieve a respectable outcome, notwithstanding several plot twists, but we expect more difficulty in the coming year.

Many historic recession indicators continue to sound the alarm, and with the consecutive quarters of GDP decline, we may already be at the beginning of a recession. Could the P&C industry be an outlier while the overall economy struggles to find the right direction?

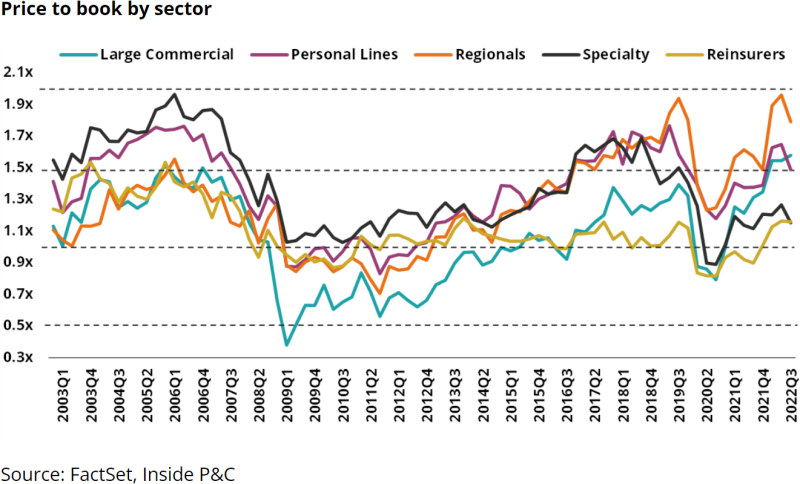

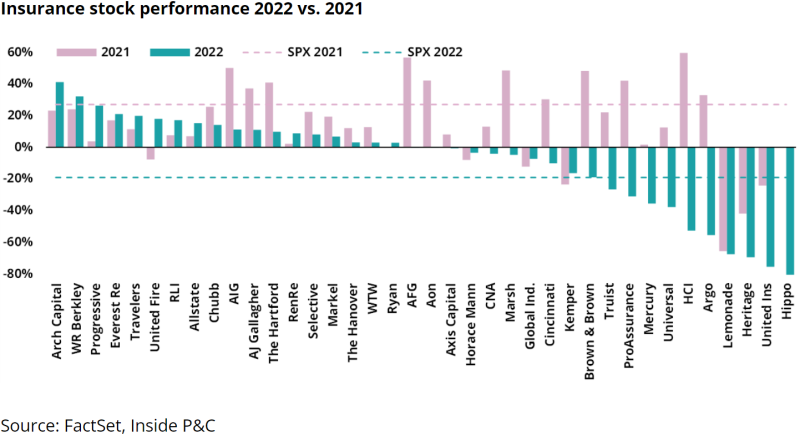

If stock price is one proxy, the insurance space has fared well post-Covid as shown below. However, part of the improvement is attributable to the decline in book value over the year, not just increasing stock price.

Taking a step back, when looking at the broader space, the individual stock prices for the companies followed the sector trends shown above (mostly). As is often the case, the long-term value creators led the group, while InsurTechs and Florida domestics lagged.

In summary, 2022 turned out to be a decent year on balance, but we expect some problems to rise to the surface in 2023. As a result, we are incrementally negative on the overall industry. The only pocket of positivity might prove to be in personal auto results.

Immediately below, we outline our high-level take on each sub-sector.

Commercial

Commercial lines pricing declines did not materialize to the level we had anticipated, buoyed by pricing, an economic recovery, and inflation; E&S and specialty were even better. Although discussed a tad more in the second half of 2022, social and loss cost inflation did not pressure underwriting results to the extent feared. There are two possible outcomes for 2023: either the industry will have a solid year when all the double-digit rate is earned, or social inflation, loss cost inflation, and a slowing economy will intersect with flattening pricing. We believe the second outcome to be more likely.

Reinsurance

Should we celebrate the news? The January 1 cat treaty renewals were one of the toughest for quite some time. Exits, large cat losses, the need for rate adequacy and trapped capital all pressured rates to unheard-of levels. The focus should be on April and July renewals at this stage, and in our mind there is a question mark over whether this discipline will last into mid-year.

Personal

Recent months have shown some evidence that personal auto players are finally beginning to get ahead of loss cost trends, albeit after several failed attempts. External forces such as supply chain constraints, used car pricing, repair, and wage inflation seem to show signs of leveling off. The odds of personal auto players getting it wrong a third time are low, so we’ll likely witness a slow recovery.

InsurTech

Drip, drip, drip. InsurTechs continue to fight a slow fall into irrelevancy, adding up to no more than residual noise in the industry. This could be the year where trends show an overall reversal. On the flip side, an industry flush with capital could look to skim the top for any players worth a lifeline.

Brokers

Brokers managed to lengthen the super-cycle beyond our expectations over 2022, benefiting from broader economic and inflationary trends. With the Fed continuing to tighten its grip to tame an overheated economy, any shift would have a negative first derivative impact on this space.

Florida domestics

Last month’s legislative changes might be too little, too late for several carriers. The recent failures, large losses, impact of fraud, and runaway attorney costs have brought structural problems with this marketplace.

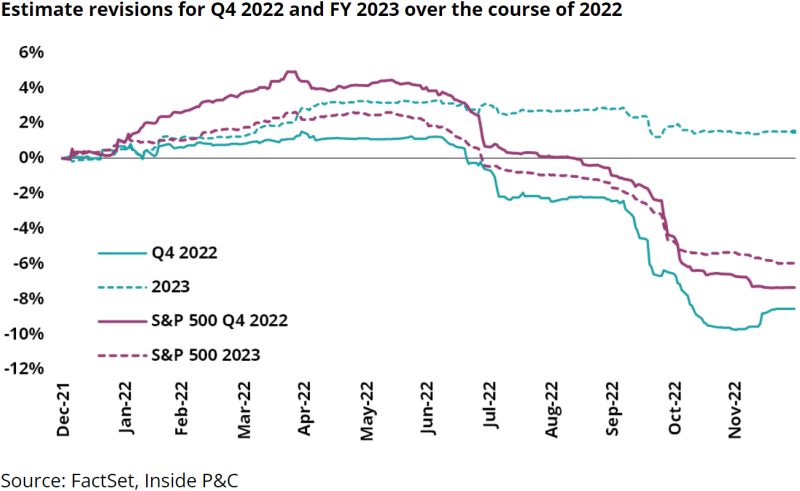

Going back to our earlier points on the industry overall, the chart below shows the group's earnings estimate expectations for 2023. Again, what stands out is that the insurance industry earnings estimates have trended down modestly (staying positive) while the S&P 500’s 2023 estimates are down close to double digits.

This implies the sector could be setting itself up for disappointment if the ROE expansion from prior years’ rates is offset by a change in loss cost trends.

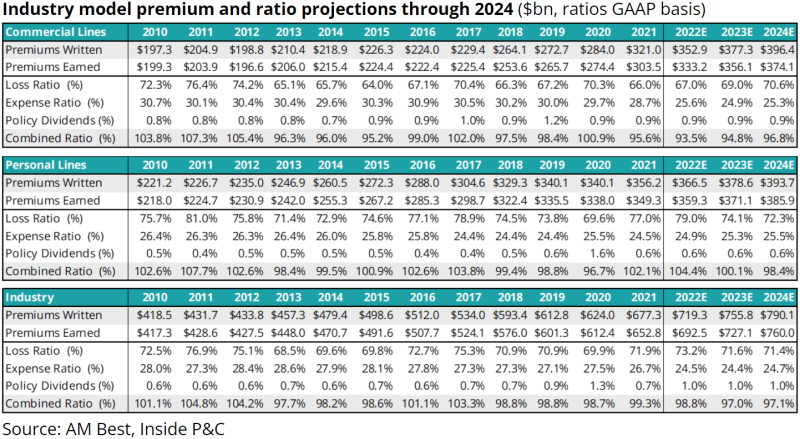

Industry model projections – Personal lines improvement to offset commercial deterioration

We have updated our industry model for 2022-2024. Our industry projections call for the industry combined ratio to be 98.8% for 2022, 97.0% for 2023, and 97.1% for 2024. Our personal lines projections are for a combined ratio ticking up to 104.4% for 2022, turning nearly breakeven for 2023, and then swinging to an underwriting profit for 2024. Our commercial lines projections are 93.5% for 2022, moving up to 94.8% for 2023 and 96.8% for 2024.

What did 2022 bring?

2022 started with a muddled outlook from the Omicron variant and its impact on the economy. What was less anticipated was the aggressive role of the federal reserve in taming inflation. This interacted with the usual property casualty sub-sector mini-cycles and buoyed some sectors while negatively impacting others.

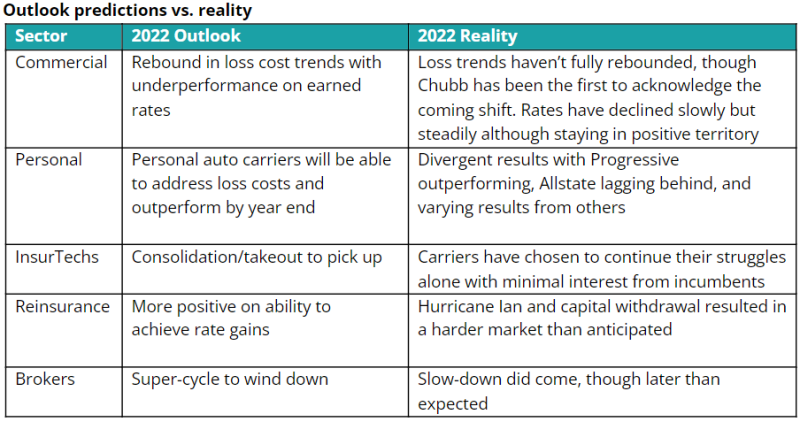

The table below shows our initial take from our 2022 outlook vs. the reality. Again, taking a step back, we were less optimistic about commercial and more optimistic about personal auto players going into 2022.

2023 timeline: Our take on how 2023 might shape up

H1: Hanging tight

January: Significant pricing gains from the cat treaty reinsurance renewal will be lauded. That said, undeployed capital and capital on the sidelines can only last so long by earning a 0% rate of return.

February: The Q4 reporting season should continue to debate pricing momentum and shifts in loss-cost trends. The focus would be on any positive Hurricane Ian loss development, the impact of Winter Storm Elliott and loss cost expectations. In addition, expect some carriers to sound the alarm on future trends as the Fed continues to increase interest rate. The focus will also be on continued unrealized losses impact on capital and the impact on higher net investment income.

March: Reserve analysis on US statutory reserves is likely to start showing a difference emerging between optimistic carriers and carriers who maintained reserving conservatism. With a recalibration of capital, expect more discussion on consolidation.

April/May: Reinsurers will try to prolong the strong momentum from January 1 renewals as they look to the April and June renewals. We remain concerned over reinsurers being able to stay on the sidelines in a harder market if capital levels recover, and believe they will likely blink first. The Tropical Meteorology Project at Colorado State University will release the season forecast in April. The tropical storm risk forecast for December 2022 has called for below-normal activity for 2023. On personal lines, companies still reporting adverse trends likely have structural issues. InsurTech results will demonstrate if they completely slip off the cliff of relevance.

H2: Negative data points might start emerging here

June: The start of the North Atlantic hurricane season will once again bring back the discussion on exposures and probable maximum losses. Also in focus will be Florida participants, or whatever remains of them at that point. The recently concluded Florida legislative efforts will be tested over the next several months.

July/August: The anticipation (or apprehension?) of the annual Monte Carlo rendezvous will begin. Reinsurers will assess the outcome of the January and mid year renewals and begin early planning for 2024. Social and loss cost inflation will continue to tick up on the commercial side.

September: Initial indications from Monte Carlo will outline the remainder of the year related to reinsurance pricing, third-party capital, and shifts in incumbents’ posturing on capital.

October/November: Pressure on rates will intensify on the commercial side. Personal results will start showing improvement at this point.

December: Reinsurers and cedants gear up for the key January 1 renewals. In the absence of an active hurricane season or other major cat losses, reinsurers will face pressure to flatten rates.

Below we discuss these sub-segments in greater detail:

1. COMMERCIAL LINES: With the economy slowing and loss trends worsening, peak pricing is behind us

On commercial lines, a tale of two cities will likely emerge, with specialty-oriented names performing better over 2023 compared to plain vanilla commercial lines.

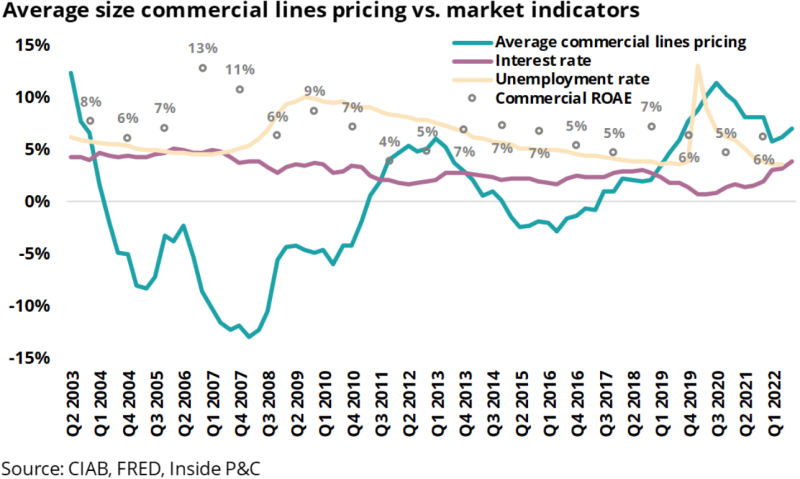

The theme of 2022 was pricing, pricing, and pricing. The chart below shows an interesting correlation. A common perception says that higher returns should follow periods of higher pricing.

But that is not always the case. The loss-cost inflation trajectory remains unknown as the industry continues to divine the Federal Reserve’s moves over 2023.

The same also goes for the overall economic situation. For example, when the economy is in a recovery phase, and employment numbers are strong, claims inflation generally does not rear its head.

If the Fed’s attempts to slow down inflation have the intended effect of strangling growth and employment, and if this shift intersects with resurgent social inflation, returns over 2023 could diverge from anticipation.

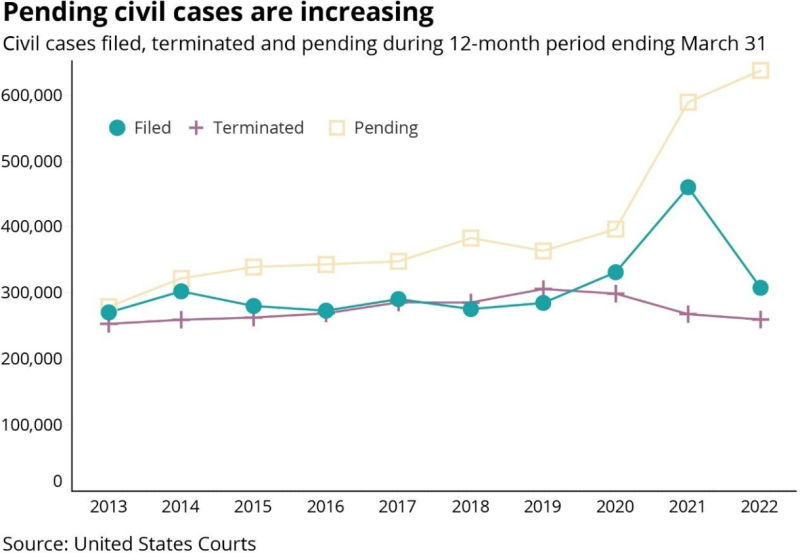

One of the outliers for 2022 has been the lack of the anticipated resurgence in social inflation. The table below shows the pending cases as a proxy for social inflation.

We continue to ask the same question – will the payout patterns diverge materially vs. anticipated when setting reserves? If the economy stumbles, it's likely that social inflation will pick up rapidly and could surprise the industry.

Taking a step back, we remain cautious about macroeconomic pressures on this industry even if rates/pricing remain positive over 2023.

The only partial offset to continue working its way through 2023 would be the improvement in investment income from rising interest rates. However, we would caution that, depending on portfolio duration, it will take several years before this shows up in returns for the industry. Additionally, we still have PTSD from prior cash flow underwriting cycles.

There is also a likelihood that some companies would be willing to bank on investment returns and continue to pursue top-line growth.

On the plus side, E&S will likely take longer to reflect the same macroeconomic pressures. As we showed in our previous note, E&S carriers have historically grown in harder markets. For disciplined E&S insurers, firming markets present an opportunity for growth.

Currently, in these more difficult times, as the more “commodity-type” broader commercial writers shrink their exposures, E&S writers are positioned to deploy capital and provide coverage at higher rates.

Moreover, we may see more insurers increase their E&S footprint. Even if they may have missed the prime opportunity that the last several quarters have presented for the specialty carriers, we may see insurers acquire E&S insurers and/or scale up their E&S operations.

2. PERSONAL LINES: Fool me thrice, shame on all of us

Personal lines insurers, particularly personal auto companies, have reason to be cautiously optimistic for 2023. While homeowners might see stabilization or even lowering of rates caused by a recession, the loss costs should be tempering.

For auto insurers, the combination of rate-taking and loss-cost stabilization should provide relief to their loss ratios. However, as detailed in a recent note, the insurers that stayed ahead of trends will look to capitalize and grow in these conditions, whereas others stay defensively positioned, playing a game of catchup.

Personal lines is segmented into auto insurance (making up 35% of industry premiums) and homeowners (making up 15% of industry premiums). This distribution has been steady for 10 years. Accordingly, auto insurance results weigh more heavily on overall personal lines.

Personal auto insurers, who enjoyed the low loss ratios afforded to them by the Covid pandemic, have faced many challenges over the past few years. Some of them were self-inflicted, while others were external.

These include changes in driving behavior, shifts in medical and vehicle parts/wages inflation, supply chain disruption worsening used car pricing, and regulatory reticence on personal auto rate adequacy.

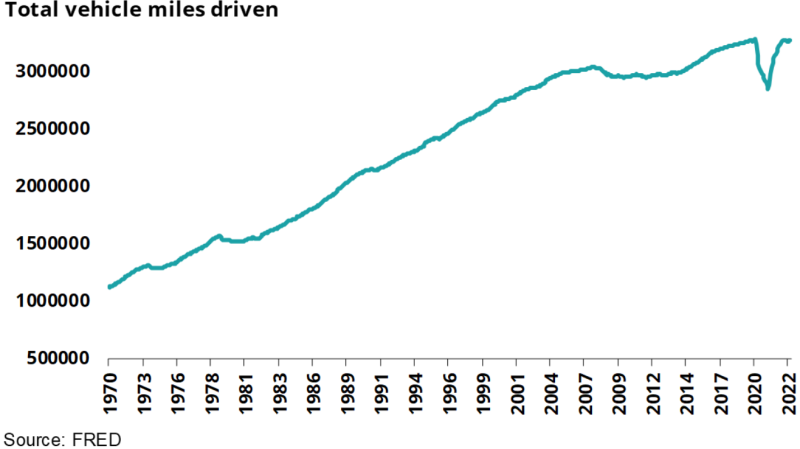

As the chart below shows, miles driven has rebounded, albeit with the driving behavior different to pre-pandemic as drivers got used to emptier roads and highways.

The graph below shows miles driven in the US for the past 52 years.

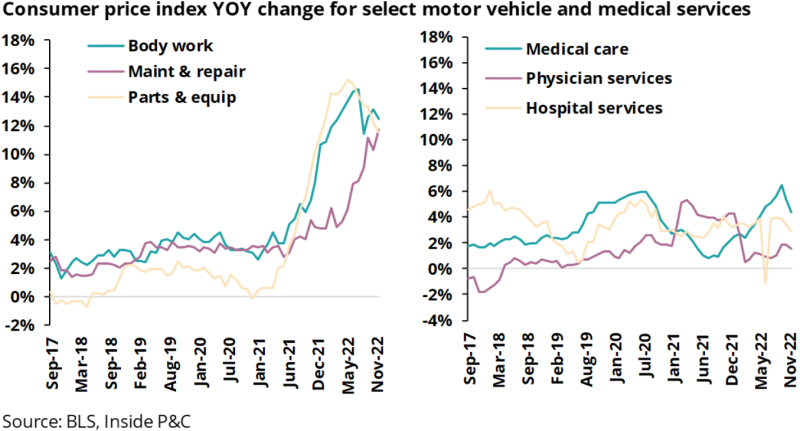

Compounding this change was the shift in loss cost trends over time which are beginning to show some signs of easing up but remain elevated compared to historical trends.

The most dramatic spikes to loss costs might be past, but auto insurers will remain cautious.

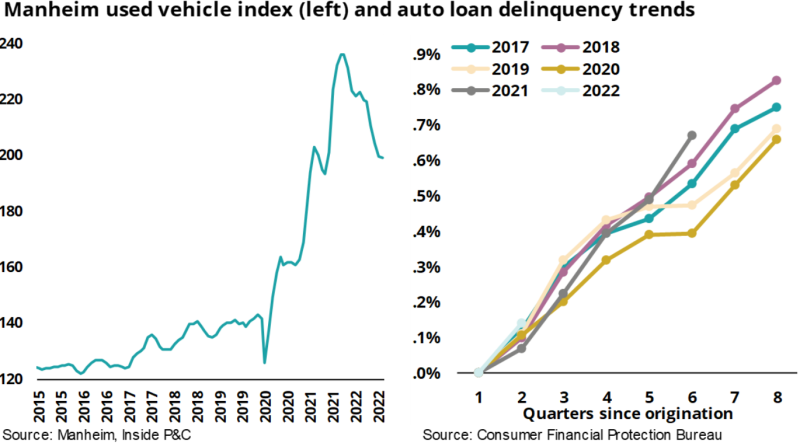

Another indicator of auto loss costs is used vehicle pricing and auto loan delinquency which, based on recent trends also look favorable vs. 2021.

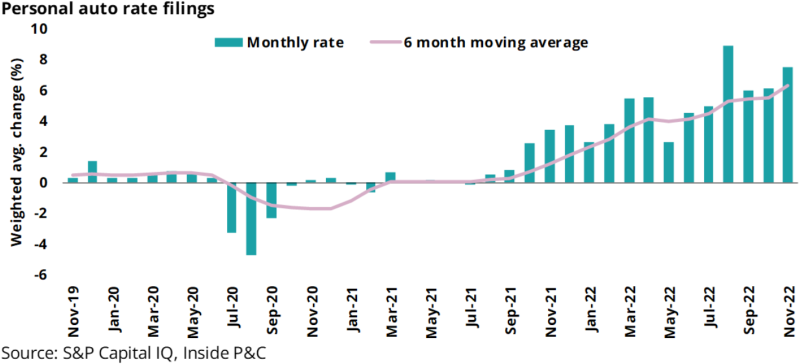

If we were to rewind back to year-end 2021 and early 2022, it would have appeared that personal auto companies were getting on top of loss cost trends. However, trends worsened, and personal auto companies had to press the rate accelerator harder.

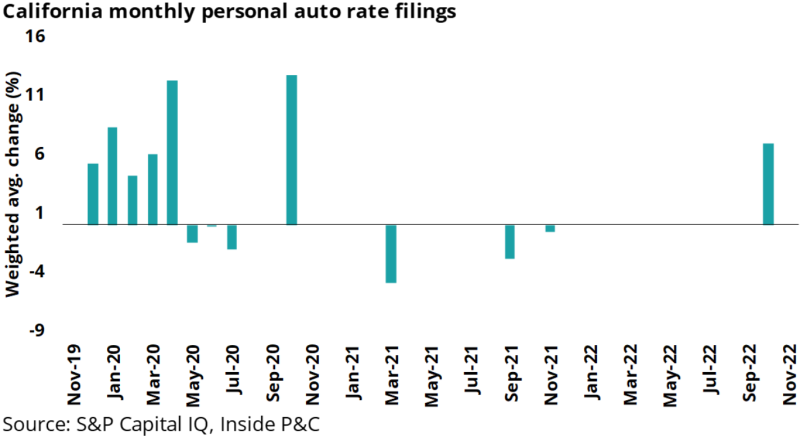

The following graph shows the weighted average rate change taken by auto insurers over the past three years.

The pandemic levels which gave auto insurers excellent results and led to a brief period of rate reduction and flattening, have given way to a dramatic increase in rates that seems only to be rising.

In recent months we have also seen states soften their attitude towards rate increases, including California, allowing several companies to take up rates in December after a lull of two years.

California represents 12% of nationwide auto premiums, so this should assist insurers that are more highly exposed to the state.

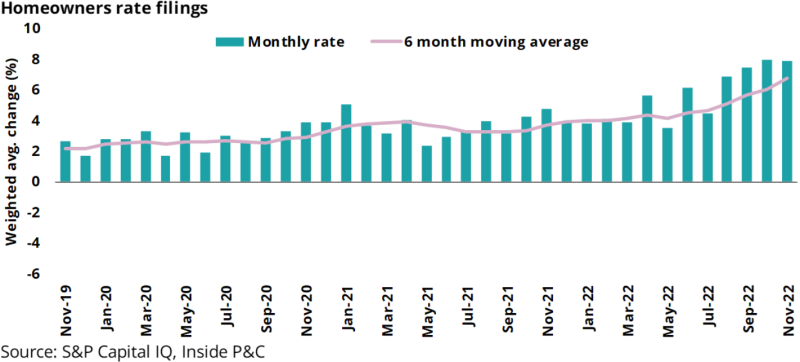

Turning to homeowners’, this sector’s exposure base has not undergone the level of volatility seen in auto insurance. Also, homeowners’ rates tend to “automatically” scale with loss costs as homeowners’ insurers have inflation-guards in their rating plans.

Inflation-guards notwithstanding, homeowners’ insurers have steadily taken necessary higher rates for the past 3 years.

The homeowners’ component of personal lines books should provide some stability as a counterbalance to the more volatile auto books.

The outlook for personal lines carriers should improve, especially for those who have learned from the volatility experienced in the past few years.

3. REINSURANCE: The New Year’s rate party will lead to increased pressure to deploy capital

Initially, 2022 was a quiet year for reinsurers, with the only blip on the radar being the Axis exit from property reinsurance in June. However, this has quickly changed over the past few months.

Now, reinsurance, and the hardening of the property-catastrophe market, have been focal points on every carrier call. With the losses from Ian and dwindling capacity, January 1 renewals this year were the most difficult many carriers have ever faced.

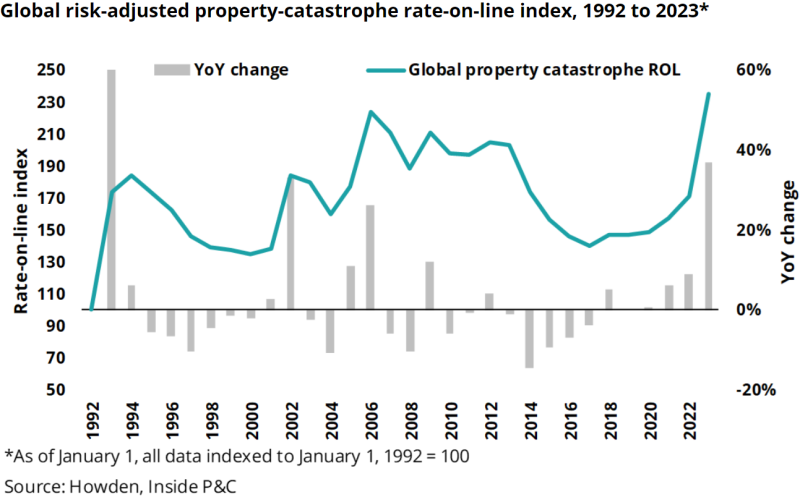

The chart below shows the global property-catastrophe rate-on-line (premium divided by limit) index over the past 30 years. Note the major upswing as the predicted market hardening has played out. Rates increased 37%, in a historic rise not seen since the post-9/11 boom 20 years ago.

This was generally predicted by the industry, after successive years of major catastrophes and other factors gave reinsurers the upper hand in January renewal negotiations.

However, while everyone is caught up on this reinsurance party, the industry may have lost sight of the bigger picture. At the end of the day, January renewal rate change is just one piece of the puzzle, and while a bump of this magnitude is clearly a plus, the additional rate may have other implications not yet considered. These renewals are now yesterday’s news, and as we get to April and July renewals, we expect to see a new issue arise as a prospective market recovery will create complications.

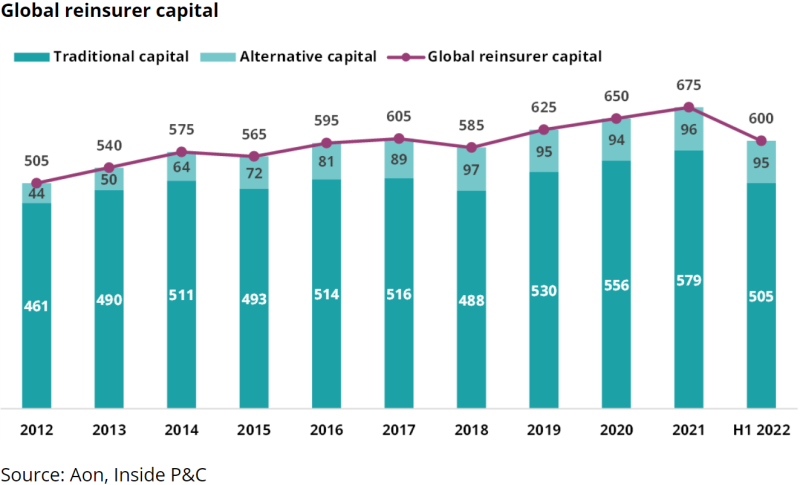

Taking a step back, despite the recent catastrophes, capital has not been significantly depleted. The chart below shows the level of capital for the reinsurance industry through H1 2022 (albeit with less opacity over the levels of alternative capital shown, where trapping is difficult to determine). Hurricane Ian and Winter Storm Elliott will add to this drop, but not enough to significantly change the situation.

In addition, the 11% drop between year-end 2021 and H1 2022 is largely reflective of investment losses rather than catastrophe losses, which is an important distinction. Unlike with cat losses, if the market rebounds, the capital will rebound with it. Whether or not this happens, with increasing rates and business booming, reinsurers will see an increase in their capital.

While this is of course a good thing, capital sitting around earns no money, and we can expect reinsurers to be under significant pressure to deploy capital, because anything is better than zero gains.

However, since January renewals are through, this pressure will coincide with later renewals, particularly the Florida renewals in June. These are the exact renewals carriers had been claiming they would pull back on.

With years of successive major catastrophes topped off by Ian, Florida domestics are the last people reinsurers want to be partnering with during a “sellers’ market” when they have the room to choose the most profitable business.

It remains to be seen if the posturing will turn into action, or if they will give in and renew the business they have said they will step away from.

4. INSURTECH: I always feel like no one’s calling me

The 2023 outlook for the InsurTechs will be one of survival, rather than the growth stories that were initially pitched to investors. The promise of disruption in the insurance industry has not panned out how it was supposed to. Instead, we have seen a mix of stubbornly high loss ratios, technologies that haven’t delivered, unsustainable cash burn, and aggressive distribution resulting in poor risk selection.

However, the legitimate problems that the InsurTechs seek to solve – individualized risk-based pricing, loss mitigation, painless purchase interface and more efficient claims-handling – will remain and those who are furthest along could succeed, in the long-term, even if it requires acquisition to get to the finish line.

With limited cash on hand, the InsurTechs’ need for capital injections is higher than ever before. This need is exacerbated by macroeconomic conditions limiting that capital's availability.

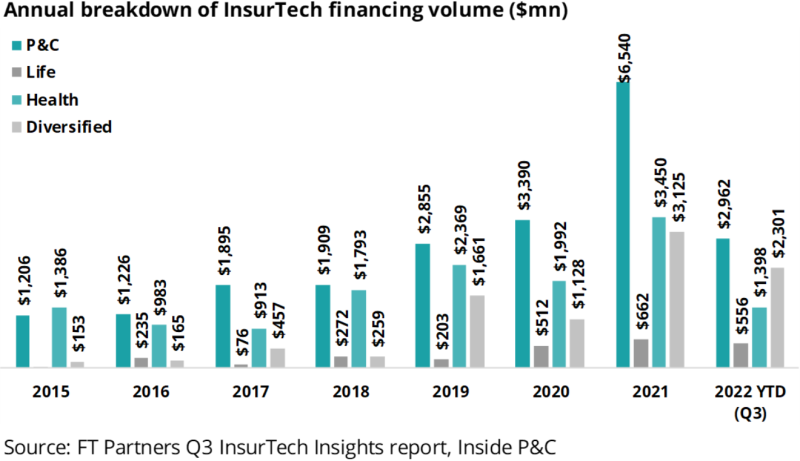

The following graph shows the source and size of InsurTech financing for the past seven years through the third quarter of 2022.

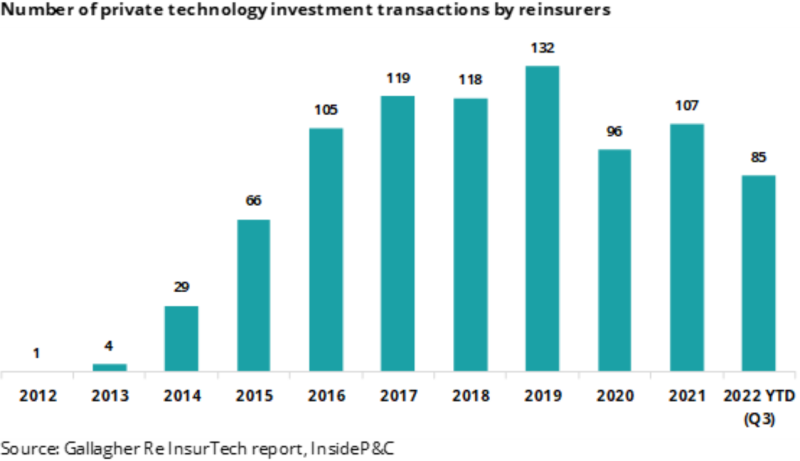

Continuing with the story surrounding InsurTech financing but focusing on reinsurers, we see that the private investments by reinsurers peaked in 2019, before the overall peaks in 2021, as shown above.

Although there is a bit of an uptick in 2021, the investment transactions from reinsurers have been trending down, and given the unfavorable re-insurance conditions in the InsurTech treaties, 2023 will likely see a continuation of this downtrend.

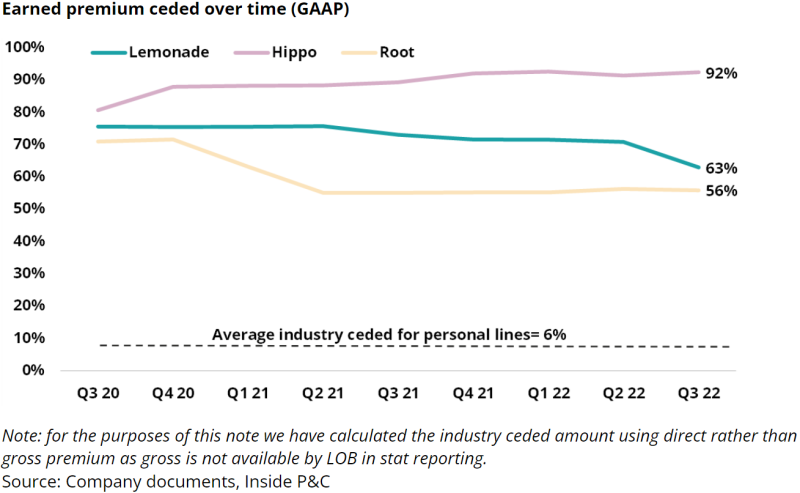

On the theme of survival, InsurTechs’ ability to cede risk to reinsurers is in serious jeopardy. Because the InsurTechs’ books are smaller, their outsized gross loss ratios lead to even larger net loss ratios. This might be a small piece of a reinsurer’s pie, but the poor performance of the InsurTechs’ books will lead to reinsurers charging significantly higher rates-on-line or choosing to withdraw capacity altogether.

The following graph shows InsurTech ceding percentages to the industry.

The only saving grace for many InsurTechs would be a potential partnership or takeout in publicly traded domains and the waiting-in-the-wings crowd.

With the overall capital level for the industry strong, incumbents may be willing to look at InsurTechs as potential acquisitions in 2023, compared to 2022 when they were more focused on organic growth.

Even then we expect to continue to see announcements of winddown, layoffs, and strategic reevaluation as not every InsurTech will find a lifeline.

5. FLORIDA: The market will continue to erode, but some players will make it through

Florida was the sector to watch these past few months, first because of the deterioration of the marketplace and the Demotech news, and then with Hurricane Ian.

Even though it is no longer hurricane season, we can expect this sector to continue to be a hot topic, as legislators attempt to hold together the last shreds of the market, insurers finish their tallies of Ian damages, and we finally get to see which Florida domestics are left standing.

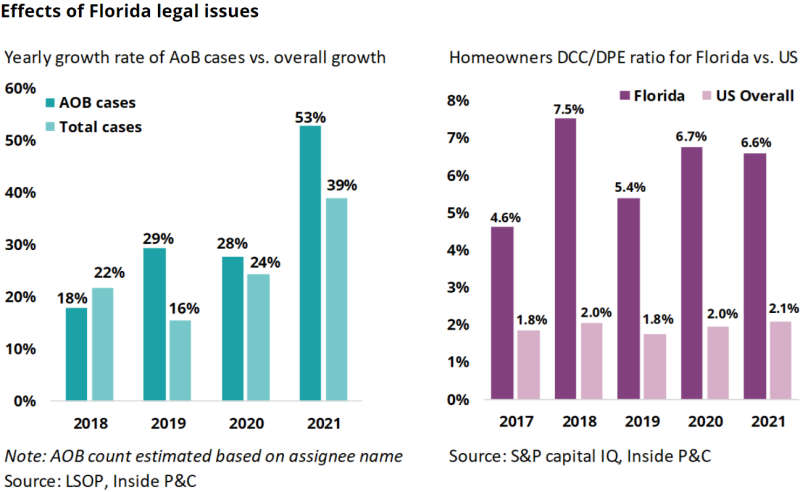

Florida legislators recently pushed through the largest overhaul in nearly 30 years, eliminating AOB and one-way attorney fees. Previous regulatory action had attempted to mitigate some of the issues without eliminating them, and, as we said at the time, it was likely too little, too late.

The charts below quantify the issue being addressed. On the left, we can see that AOB cases have been growing steadily, and much faster than the total case load. On the right is the ratio of defense and containment cost to direct earned premium. Over the last several years, we can see that Florida is paying more than three times as much per dollar of premium in defense costs as the US in general.

While this new complete elimination may no longer be too little, it may still be too late, as many companies have already been forced to exit, are in receivership, or are on the brink of collapse.

It also remains to be seen if the measures work, or if bad players will find a way around them.

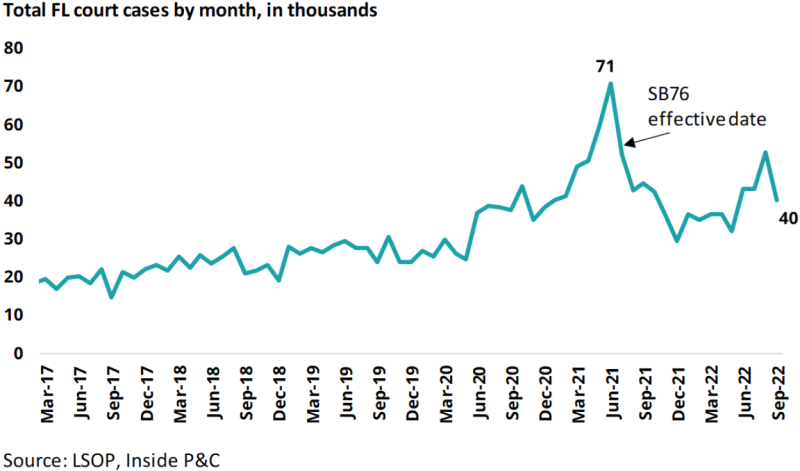

The chart below shows Florida court cases over time. Note where Senate bill 76 (SB76) took effect.

While it did drop the number of cases significantly, two things stand out. First, it initially resulted in a peak as people tried to get their cases in before the new law would take effect. And second, even though it caused a massive drop off, the resulting numbers are still historically high, and were beginning to peak again.

While these latest steps are stronger than SB76, we still expect it to have these before-and-after effects – capitulations the fragile market can’t take.

Overall, our outlook is pessimistic here, and while we expect to see some benefit from the removal of predatory legal practices for the remaining companies, even a complete success on that front would take a while to cycle through and stabilize what is left of the market.

6. BROKERS: The super-cycle will end, but broker results will still be positive

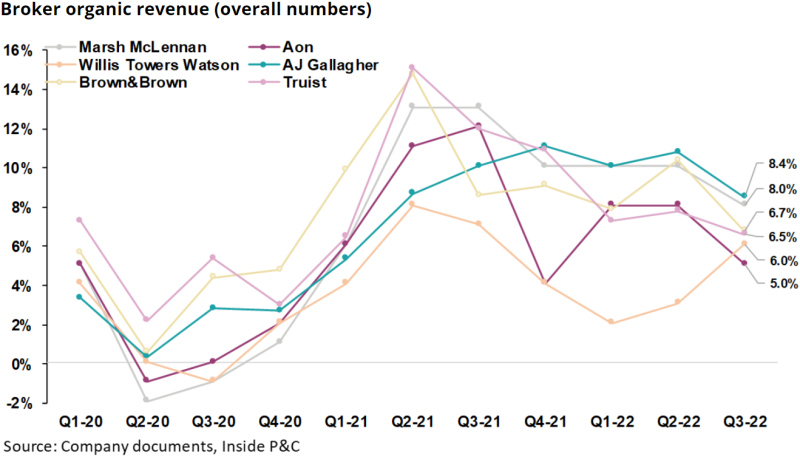

Brokers have been the star sector of the past year, as the super-cycle that propelled them through 2021 defied expectations and continued through 2022. However, eventually it did begin to wind down.

As we noted in our Q3 broker earnings piece, these numbers are only “down” with respect to the highs of the super-cycle, and are still positive and historically quite high.

The chart below shows organic revenues over time. We can see the clear upswing to the Q2-21 peak followed by the winding down over the last six quarters.

Despite the difficult macroeconomic backdrop mentioned on every earnings call this past year, the brokers managed to not only survive but thrive.

This is because of two things. First the rate environment, which has grown tremendously, feeds directly into broker revenues. Second, inflation increases premiums and therefore commissions and fees for the brokers.

While the rate environment is cooling, inflation has still been at historic highs, enabling the soft landing we are seeing with the cycle.

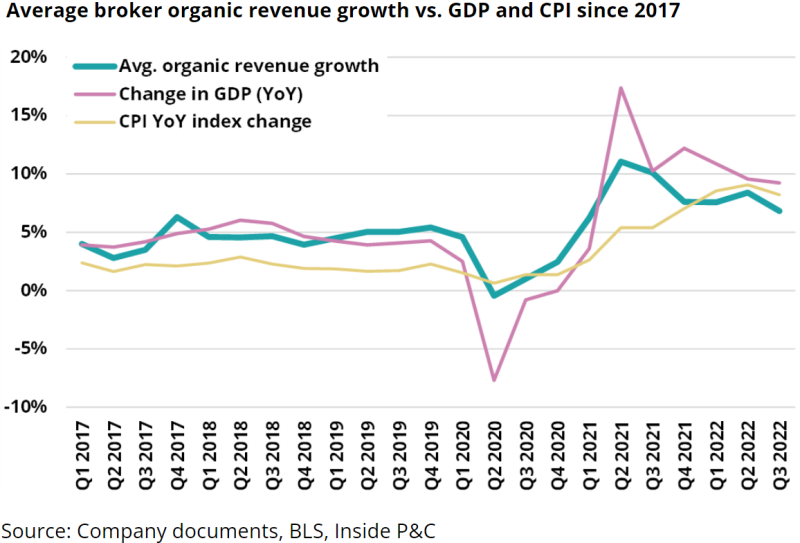

The chart below shows the average broker organic growth against the economic indicators of CPI and GDP. We can see they move in lockstep, so the environment in 2023 will be the main factor in predicting broker success. As these tailwinds begin to lag, we should expect organic revenue to go back to a more normal cycle.

The other factor to keep in mind is that brokers benefit from the various sub-cycles of the other segments. Though we aren’t overly optimistic on continued reinsurance rate growth, the January 37% increase may give a boost to more reinsurance-heavy brokers like Aon.

This sector may see some shakeups as well. First, Truist has reportedly hired Morgan Stanley to explore a sale of up to 30% of its insurance brokerage unit. Second, new Marsh McLennan CEO John Doyle officially took charge on January 1, and while he has said he intends to stay the course keeping business largely as-is, it remains to be seen how he may be forced to change that tack if tailwinds peter out.

Overall, this should be an interesting year for the broker sub-group. We expect to see continued growth, though an end to the double digits, but still expect a strong performance.

In summary, we expect 2023 to be an incrementally negative year for commercial carriers, brokers, reinsurers, and InsurTechs. However, on the positive front, personal lines, particularly personal auto, will be incrementally better as rate increases start getting earned as some of the prior negative factors begin to ease up.