State Farm

-

The commissioner said more work needs to be done, but big companies are interested in coming back.

The commissioner said more work needs to be done, but big companies are interested in coming back. -

Carriers underweight in E&S could lead the charge in the next round of M&A.

-

The Republican said his office has launched an investigation into the denials.

-

The ratings agency said that it continues to assess State Farm’s balance sheet among the strongest.

-

State regulators have largely avoided enforceable AI regulations, but bad news could change that.

-

The regulations are designed to address long-term solvency concerns.

-

State Farm is under investigation as its premiums have been rising “drastically".

-

IBHS CEO Roy Wright says insurers need a comprehensive approach to resilience.

-

Roughly half a year since the LA fires, brokers said there’s hope things are turning around.

-

The class can collectively challenge State Farm’s property claims calculations.

-

The ruling comes as insurers face growing legal pressures following the January blazes.

-

Lara approved an interim rate increase for the company just weeks ago.

-

The company seeks the full 30% homeowners’ rate request it made last June.

-

State Farm will need to provide its CA subsidiary with a $400mn surplus note.

-

The carrier has received 12,300 claims as of 28 March.

-

Commissioner Lara also proposed a $500mn cash infusion from parent State Farm.

-

The carrier has also received 11,750 fire-related claims so far this year.

-

The company is seeking an emergency rate increase after the devastating Los Angeles wildfires.

-

State Farm General has asked California regulators for an emergency rate increase.

-

The carrier has paid $1.75bn on around 9,500 claims filed from the wildfires.

-

Sources said California regulators need to show they’re receptive to private insurer needs.

-

The insurer is seeking a 22% interim raise, but the request is currently on hold.

-

The insurance commissioner said the carrier has not shown the need for price increases.

-

The insurer disclosed the estimates as it seeks emergency rate hikes from regulators.

-

The company says the recent wildfires will be the costliest in its history.

-

The carrier has around $2.5bn-$4bn of reinsurance cover specifically for California risk.

-

The company received over 10,100 home and auto claims as of January 27.

-

A state-mandated, one-year moratorium on non-renewals is also in place.

-

Insurers are fighting to recoup claims they have paid out.

-

Independent litigation threatened a $4bn settlement with wildfire victims.

-

The victims claim insurers shouldn’t get settlement cash before they’re made whole.

-

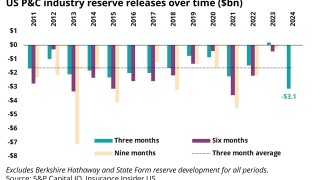

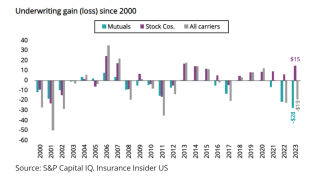

The discrepancy between rising claim counts and favorable reserves is cause for concern.

-

Mutuals struggle to react and adapt to a worsening loss environment.

-

The downgrade reflects the company’s balance sheet strength, which AM Best assessed as weak.

-

The carrier stopped accepting new HO business in the state last May.

-